Is Waterways Leisure Tourism IPO Good or Bad – Detailed Review

00:00 / 00:00

Summary

| ||

Waterways Leisure Tourism Limited’s IPO is set to open its initial public offering from June 23, 2026, to June 25, 2026. When considering applying for this IPO, potential investors might have questions about whether the Waterways Leisure Tourism IPO is a good investment and if it's worth subscribing to.

This article provides a comprehensive analysis of Waterways Leisure Tourism's IPO, covering its business operations and a fundamental analysis of its RHP to help you make an informed investment decision.

Waterways Leisure Tourism IPO Review

Waterways Leisure Tourism Limited IPO is open for subscription from June 23, 2026, to June 25, 2026, with listing expected on July 01, 2026, on NSE and BSE.

The company operates as a pioneer of domestic ocean cruises in India, launching its premium brand 'Cordelia Cruises' in 2021 with its first premium ship, the 'MV Empress' (acquired via BVI subsidiary Bay Cruise Investments Inc.).

The company blends world-class hospitality, gourmet dining (including specialized Jain cuisine), and grand thematic Indian entertainment shows to cater to families, couples, and corporate MICE events.

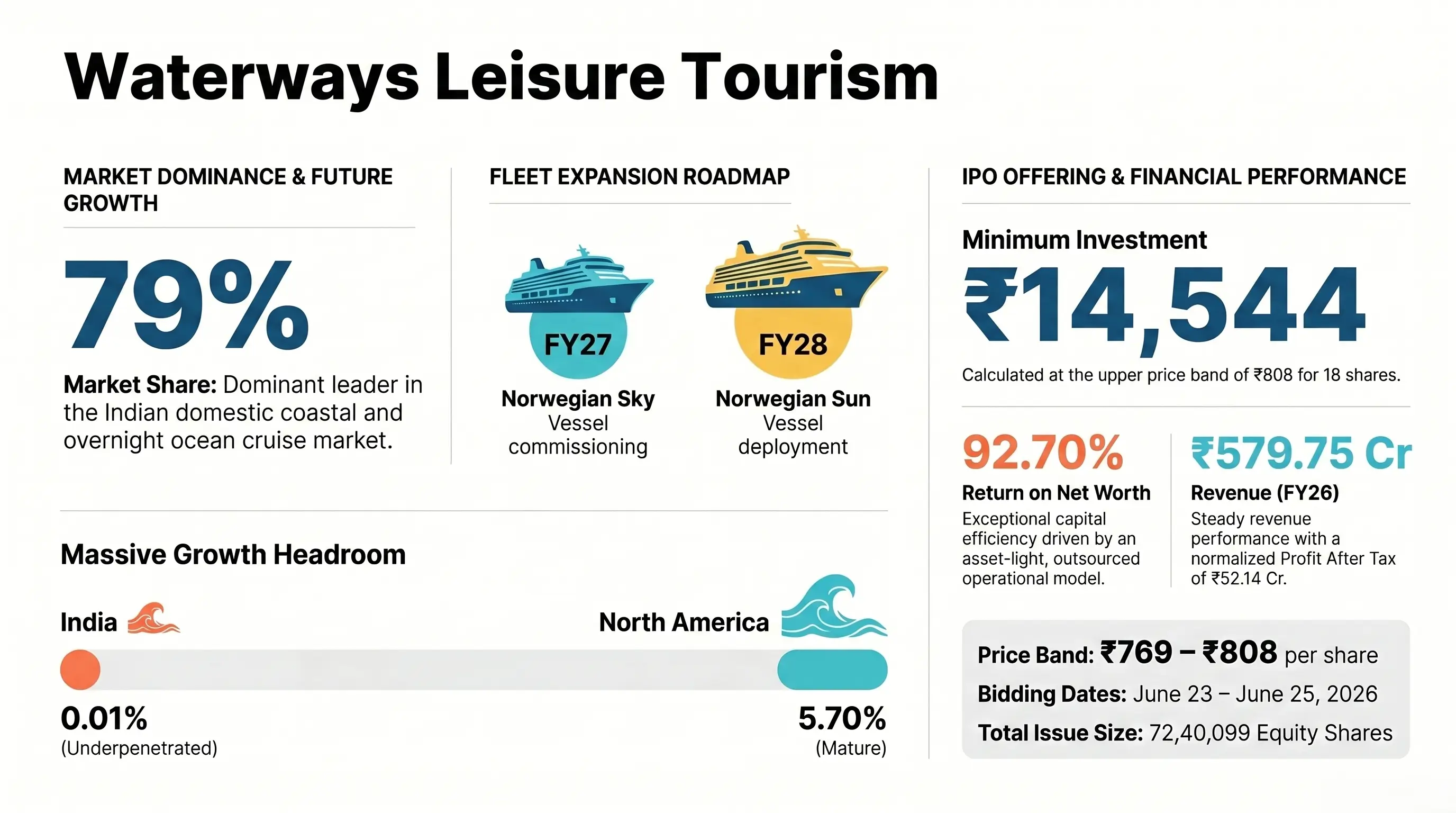

As of the fiscal year ended March 31, 2026, the company reported revenue from operations of Rs 579.75 crore, driven by a robust guest-carrying footprint of 730,819 passengers since its launch.

Waterways Leisure Tourism is strategically positioned to capitalize on a massive domestic overnight cruise dominance, holding an exceptional 79% market share in value terms in Fiscal 2025 (according to the CRISIL Report).

The company’s operations are supported by a strong domestic presence at key Indian homeports (Mumbai, Chennai, Kochi, Goa, Visakhapatnam, and Lakshadweep), alongside international sailings to Sri Lanka, Thailand, Malaysia, and Singapore.

Its revenue from operations grew from Rs 444.06 crore in FY24 to Rs 590.61 crore in FY25, before slightly moderating to Rs 579.75 crore in FY26.

For the year ended March 31, 2026, the company reported a Profit After Tax (PAT) of Rs 52.14 crore. This follows an exceptional net profit of Rs 168.19 crore in FY25 (which was propped up by a non-recurring lease derecognition exceptional gain of Rs 75.59 crore).

The company maintains healthy operational metrics, with an EBITDA margin of 20.26% and an exceptional Debt to Equity ratio of 1.27 times as of March 31, 2026.

Key strengths include its integrated operations, pioneer brand positioning ('Cordelia Cruises'), optimized direct-to-consumer booking channels, and an asset-light vessel leasing model.

Primary risks include a high geographic concentration at Mumbai Port, single-vessel dependency on the 'MV Empress', extreme sensitivity to global fuel price fluctuations, and outstanding tax/regulatory disputes.

The book-built issue consists entirely of a Fresh Issue of up to Rs 585.00 crore, meaning all proceeds will flow directly to the company to fund fleet expansion, and there is no Offer for Sale (OFS).

Shares are priced in the Waterways Leisure Tourism IPO price band of Rs 769 to Rs 808 per share, with a minimum lot size of 18 shares.

What does Waterways Leisure Tourism do?

Waterways Leisure Tourism operates as a differentiated pure-play leisure tourism company. It manages premium shipboard hospitality, maritime transport, and curated shore excursions to address growing domestic discretionary spending.

The company utilizes its specialized, customized cruise operations to formulate an authentic, "India-focused" premium high-sea holiday experience.

This operational cycle is carried out in three main steps:

Step 1: Booking Engine Optimization: Cabins are sold directly through their custom website, mobile app, and in-house call centers staffed by 148 cruise holiday experts (62.25% of cabins sold in FY26), alongside strategic B2B travel agent integrations.

Step 2: Port Embarkation & Ground Logistics: Streamlined guest handling, security checks, and baggage handling are conducted at homeports in cities such as Mumbai or Chennai using temporary or dedicated terminal spaces.

Step 3: Onboard Premium Hospitality & Curated Entertainment: Guests enjoy full-board dining, luxury accommodations, Broadway-scale stage performances, casino access, and customized shore excursions at various domestic and international ports of call.

Waterways Leisure Tourism, through its maritime operations, commands a leading presence in India, with its primary vessel, the 'MV Empress' (796 cabins, carrying capacity of 2,005 guests), in active service since September 2021.

The company handles the entire lifecycle of cruise tourism development, from bunkering and route planning to safety drills and vessel technical management. They leverage multi-stage marine safety inspections under international Lloyd's Register certifications.

Waterways Leisure Tourism Business Segments

The company serves its retail, corporate, and leisure clients through three main business segments:

Revenue Segment | % of Revenue (Year Ended March 31, 2026) |

Cruise Ticket Sales (Accommodations, Basic Dining, Basic Shows) | 91.22% |

Onboard Revenue (Specialty Dining, Casinos, Spas, Excursions, Wi-Fi) | 8.72% |

Other Operating Revenue (Commission Income on Sri Lanka Excursions) | 0.05% |

Total Revenue from Operations | 100.00% |

Key Operational Features

The company’s operations are supported by a strategically optimized vessel infrastructure. They hold globally recognized maritime safety certifications issued by Lloyd's Register.

The Chairman of the Board, Executive Director, and CEO Jurgen Bailom, Executive Directors Aditya Gupta and Coralie Annamichele Ansari, alongside CFO Nishikant Upadhyay, lead the company, leveraging their extensive expertise in cruise line logistics, hospitality management, and corporate finance.

What is the market opportunity for Waterways Leisure Tourism?

Waterways Leisure Tourism Limited operates within the Indian overnight ocean and coastal cruise industry. This sector is undergoing steady growth, driven by rising discretionary incomes, the expansion of premium travel segments, and robust government initiatives such as the Cruise Bharat Mission and Maritime India Vision 2030.

The total Indian cruise market is in a highly underpenetrated stage, with cruise market penetration in India standing at just 0.01% compared to 5.70% in mature markets like North America.

This represents a substantial room for growth as domestic consumers shift spending from standard vacations towards high-value experiential tourism.

Crucially, the premium cruise and luxury resort segment remains a high-growth area as rising high-income groups (households earning more than Rs 30 lakh per annum are projected to reach 11% of the population by FY31) seek curated entertainment, destination high-sea weddings, and corporate MICE (Meetings, Incentives, Conferences, and Exhibitions) events.

Despite this potential, the industry faces persistent challenges, including high fuel price sensitivities (fuel costs were 16.49% of total expenses in FY26), unhedged foreign exchange liabilities, heavy dependency on port clearances, and complex multi-ministry tax structures such as GST on cruise tickets.

Industry statistics are sourced from the Waterways Leisure Tourism Limited Red Herring Prospectus (RHP) dated June 17, 2026.

Is Waterways Leisure Tourism Limited Profitable?

Particulars | Year Ended Mar 31, 2026 (Rs Crore) | Year Ended Mar 31, 2025 (Rs Crore) | Year Ended Mar 31, 2024 (Rs Crore) |

Revenue from Operations | 579.75 | 590.61 | 444.06 |

EBITDA Margin | 20.26% | 36.48% | 25.03% |

Profit After Tax (PAT) | 52.14 | 168.19 | -122.73 |

Return on Net Worth (RoNW) | 92.70% | 394.41% | 217.46% |

Debt to Equity (D/E) Ratio (Times) | 1.27 | 0.93 | (0.04) |

Revenue from Operations: This is the total money the company earned from its core business activities, including cruise ticket bookings and onboard guest expenditures. It shows the overall scale of the core business, which grew significantly from Rs 444.06 crore in FY24 to Rs 590.61 crore in FY25 due to a rapid post-pandemic rebound in revenge travel demand before settling at Rs 579.75 crore in FY26 as domestic tourism demand stabilized.

EBITDA Margin: This is the core operating profit shown as a percentage of revenue from operations. It tells you how efficient the company is at turning sales into operating profit. It rose to 36.48% in FY25 due to peak passenger load factors (91.63%) and lower relative fuel costs, but moderated to 20.26% in FY26 owing to rising operating costs and increased administrative expenses.

Profit After Tax (PAT): This is the actual bottom-line net profit left for the owners after paying every single expense, interest, depreciation, and tax. The company is not consistently profitable, with its PAT growing from a loss of Rs (122.73) crore in FY24 to a profit of Rs 168.19 crore in FY25, though this was heavily propped up by a non-recurring lease derecognition exceptional gain of Rs 75.59 crore, leading to a normalized PAT of Rs 52.14 crore in FY26.

Return on Equity (RoE): This measures how much profit the company generates for every rupee of shareholder equity invested, indicating capital efficiency. Driven by its lean, highly optimized, and outsourced operational framework, it reached an exceptional 92.70% in FY26, showing that the company generates outstanding returns on its net worth despite its smaller capital base.

Debt to Equity (D/E) Ratio: This ratio indicates the proportion of debt a company uses to finance its assets relative to the value of shareholders' equity, serving as a key measure of financial leverage. It stood at 0.93 times in FY25 and increased to 1.27 times in FY26 due to the acquisition of short-term facilities and working capital setups, reflecting higher leverage, which is managed by cash generated from advance cruise bookings.

Financial figures are sourced from the Waterways Leisure Tourism Limited Red Herring Prospectus (RHP) dated June 17, 2026.

Strengths and Risks of Waterways Leisure Tourism IPO

Let's examine the strengths and weaknesses to determine whether the Waterways Leisure Tourism IPO is good or bad for investors.

Strengths

Pioneering Domestic Advantage: Holding an overwhelming 79% market share in the Indian domestic coastal and overnight ocean cruise value market as of FY26.

Optimized Direct Booking Channel: Sells 62.25% of its total cabins directly through its online portal, minimizing agent commissions and driving higher operational margins.

Asset-Light Strategic Outsourcing: Minimizes heavy operational overhead by outsourcing technical management, onboard catering, logistics, and entertainment to specialized global partners (such as Wizcraft, Apollo, and SA Cruise Services).

Proven Guest Retention: Welcomed over 7,30,819 guests since its launch with a robust passenger load factor of 84.99% in FY26.

Strong Brand Moat: Built a premium brand equity under the name 'Cordelia Cruises', which is synonymous with high-sea luxury in India.

Risks

Single-Vessel Dependency: Currently, the entire revenue and maritime operations depend on a single ship, the 'MV Empress'. Any mechanical failure, containment, or port delay would halt operations.

Geographic Concentration at Mumbai: Over 67% of all cruise passengers were onboarded at Mumbai Port in FY26 (71% in FY25), making the company highly sensitive to regulatory or environmental issues in Maharashtra.

Raw Material Price Volatility: Marine fuel is a major cost component (16.49% of total expenses in FY26). The absence of a hedging mechanism exposes profit margins to sudden fluctuations in international fuel prices.

Unhedged Foreign Exchange Exposure: Heavy reliance on USD-denominated payments for port charges, charter hire, and technical services leaves the company exposed to currency fluctuations, holding unhedged receivables of Rs 47.33 crore as of FY26.

High Employee Attrition: The company faces high attrition rates among customer-facing staff, recording an attrition of 43.02% in Fiscal 2026 (40.22% in FY25).

Strategies of Waterways Leisure Tourism IPO

Introduce new cruise vessels to meet growing demand: The company plans to acquire two new cruise vessels on lease, Norwegian Sky (to be commercialised in FY27) and Norwegian Sun (to be commercialised in FY28), to expand carrying capacity and meet growing consumer demand.

Broaden itineraries to cover domestic and international destinations: Deploying the new fleet to launch exciting new coastal routes in India (such as Diu, Porbandar, Port Blair, Kolkata, and New Mangalore) and entering high-potential international waters, including the Maldives, Indonesia, Australia, the UAE, Oman, Kuwait, and Mauritius.

Waterways Leisure Tourism IPO vs. Peers

There are no direct comparisons for Waterways Leisure Tourism in the Indian stock markets because of its unique business model. However, to assist investors, the RHP provides a comparative framework grouping the company against listed Indian peers in the hospitality and entertainment sectors, alongside major global cruise line operators.

These comparative peer groups include:

Listed Indian Hotels: Chalet Hotels, Lemon Tree Hotels, Juniper Hotels, Samhi Hotels, and Taj GVK Hotels & Resorts.

Listed Indian Entertainment: Wonderla Holidays and Imagicaa World Entertainment.

Global Cruise Operators: Royal Caribbean Cruises Ltd, Carnival Corporation & PLC, and Norwegian Cruise Line Holdings Ltd.

The following securities mentioned are for comparative purposes only and do not constitute a recommendation to buy or sell.

Revenue from Operations: Shows overall market footprint. While global giants like Carnival Corporation & PLC operate on a huge scale (generating over Rs 58,716.51 crore in revenues) and Indian hospitality leaders like Chalet Hotels report larger localized footprints (Rs 2,769.75 crore), Waterways Leisure Tourism (reporting Rs 579.75 crore in FY26) represents a highly specialized, pure-play domestic competitor carving out a unique high-sea holiday niche.

EBITDA Margins: Measures core operational profitability. Waterways Leisure Tourism demonstrates healthy margins (with an EBITDA margin of 20.26% in FY26) through its asset-light vessel leasing model. However, the global peers are in the higher margin range.

Return on Net Worth (RoNW): Measures capital efficiency. Driven by its lean, outsourced operational framework and overwhelming 79% domestic market share, Waterways Leisure Tourism outperforms both global cruise operators (such as Carnival at 2.08% and Royal Caribbean at 9.37%) and premier Indian hospitality and entertainment peers with an exceptional capital efficiency and RoNW of 92.70% in Fiscal 2026 because of the low equity base effect.

Objectives of Waterways Leisure Tourism IPO

The offering consists entirely of a Fresh Issue of up to Rs 585 crore for:

Funding Advanced Lease Rentals/Deposits and monthly lease payments for its step-down subsidiary, Baycruise Shipping and Leasing (IFSC) Private Limited, for the acquisition of vessels, Norwegian Sky and Norwegian Sun: Rs 480.01 crore.

Remaining funds are directed towards General Corporate Purposes.

Waterways Leisure Tourism IPO Details

IPO Dates

Waterways Leisure Tourism IPO will be open for subscription from June 23, 2026, to June 25, 2026. The allotment of shares to investors will take place on June 29, 2026, and the company is expected to be listed on the NSE and BSE on July 01, 2026.

IPO Issue Price

Waterways Leisure Tourism is offering its shares in the price band of Rs 769 to Rs 808 per share. This means you would require an investment of Rs 14,544 per lot (18 shares) if you are bidding for the IPO at the upper price band.

IPO Size

Waterways Leisure Tourism is launching a Rs 585 crore IPO, consisting entirely of a fresh issue of about 72.4 lakh shares.

IPO Allotment Status

Investors who applied for the IPO can check their IPO allotment status on June 29, 2026, through the registrar's website, MUFG Intime India Private Limited, BSE, NSE, or through their stockbroker platform.

IPO Listing Date

The shares of Waterways Leisure Tourism are expected to be listed on the NSE and BSE on July 01, 2026.

IPO Application Link

Open demat account with Rupeezy today and enjoy a seamless experience when applying for the IPO. With an easy-to-use platform, Rupeezy makes the IPO application process quick and hassle-free.

Apply for Waterways Leisure Tourism IPO

Important IPO Details | |

Bidding Date | June 23, 2026 to June 25, 2026 |

Allotment Date | June 29, 2026 |

Listing Date | July 01, 2026 |

Issue Price | Rs 769 to Rs 808 per share |

Lot Size | 18 Shares |

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

Disclaimer

Investments in securities market are subject to market risks, read all the related documents carefully before investing . Rupeezy (SEBI RA Registration: INH000013332) provides this content for informational purposes; any securities quoted are for educational display and not as a recommendation. All charts and graphs are based on independent research and reliable sources for the period mentioned within the specific data set. Sometimes we take graphs from external sources. This communication does not promise or assure any fixed, guaranteed, or indicative returns to any client. For our complete registered office address, Member ID, and full SEBI registration details, please refer to our official website.

All Category