Is SEDEMAC Mechatronics IPO Good or Bad – Detailed Review

00:00 / 00:00

SEDEMAC Mechatronics Limited’s IPO is set to open its initial public offering from March 04, 2026, to March 06, 2026. When considering applying for this IPO, potential investors might have questions about whether the SEDEMAC Mechatronics IPO is a good investment and if it's worth subscribing to.

This article provides a comprehensive analysis of SEDEMAC Mechatronics IPO, covering its business operations and fundamental analysis from its RHP to help you make an informed investment decision.

Investments in the securities market are subject to market risks. Read all the related documents carefully before investing.

SEDEMAC Mechatronics IPO Review

SEDEMAC Mechatronics Limited's IPO is open for subscription from March 04, 2026, to March 06, 2026, with listing expected on March 11, 2026, on NSE and BSE.

The company is a technology-focused deep-tech company specializing in control-intensive electronic control units (ECUs) for automotive and industrial applications. Operating as a design-led player in the global powertrain ecosystem, it provides high-quality electronic solutions through proprietary technology platforms. As of December 31, 2025, the company serves major vehicle and industrial equipment manufacturers across India, the US, and Europe. Its core business focuses on Integrated Starter Generator (ISG) ECUs and Electronic Fuel Injection (EFI) systems, which serve as the primary drivers of its revenue.

The platform serves an ecosystem of diverse global customers through significant manufacturing operations in Pune, Maharashtra. The company leverages an engineering-first, innovation-led, and scalable manufacturing platform that integrates internal R&D with over 12 patents across regions. The company identifies Prof. Shashikanth Suryanarayanan, Amit Arun Dixit, Manish Sharma, and Anaykumar Avinash Joshi as its promoters, who collectively hold 22.26% of the pre-offer paid-up equity share capital.

The company operates within the global and Indian control technologies industry, which is undergoing a rapid transformation driven by emissions regulations and electrification. The domestic ISG ECU market is significant, with SEDEMAC holding a leading 35% market share, while it commands an estimated 75% to 77% of the Indian genset controller market. This growth is fuelled by increasing demand for sensorless motor control and cleaner industrial power equipment, particularly in high-growth segments like electric vehicle powertrains.

SEDEMAC Mechatronics’ financial performance reflects robust growth and high operational efficiency. Revenue from operations grew from Rs 423.03 crore in FY23 to Rs 658.36 crore in FY25, reporting Rs 770.67 crore for the nine months ended December 31, 2025. Profit After Tax (PAT) rose from Rs 8.57 crore in FY23 to Rs 47.05 crore in FY25, with a reported PAT of Rs 71.50 crore for the 9M FY26 period.

The company maintains competitive margins, with an EBITDA margin of 19.00% and a return on equity (RoE) of 22.01% in FY25, outperforming several established listed peers like Bosch and Schaeffler India in terms of profitability and capital efficiency.

Key strengths include its first-to-market advantage in sensorless ISG ECUs, patent leadership, and integrated operations that allow for rapid innovation. Risks involve high customer concentration (75.48% of revenue from TVS Motor), significant segment exposure to the mobility market (84.63% of revenue), and supply chain volatility regarding critical semiconductor imports from China.

The offering consists of a total book-built issue worth approximately Rs 1,087 crore, comprised entirely of an Offer for Sale (OFS) of 80,43,300 equity shares. There is no fresh issue component, meaning all proceeds will be received by the selling shareholders, including the promoters and various investment funds.

Shares are priced in the band of Rs 1,287 to Rs 1,352 per share, with a lot size of 11 shares.

Company Overview of SEDEMAC Mechatronics IPO

SEDEMAC Mechatronics Limited is a technology-focused deep-tech company that specialises in providing a wide range of control-intensive electronic control units (ECUs) for automotive and industrial applications. The company operates as a design-led player in the highly competitive global powertrain control ecosystem. It is a provider of high-quality, innovative electronic solutions through its proprietary technology platforms, serving major vehicle and industrial equipment manufacturers across India, the United States, and Europe as of December 31, 2025.

Its core business focus is on the design and manufacture of critical electronic components, such as Integrated Starter Generator (ISG) ECUs and Electronic Fuel Injection (EFI) systems, which form the backbone of its revenue.

The diversified product portfolio includes specialized technology categories primarily supplied to leading Original Equipment Manufacturers (OEMs):

Integrated Starter Generators (ISG) ECUs: A high-volume segment featuring patented sensorless commutation technology that eliminates traditional starter motors in two- and three-wheelers.

Electronic Fuel Injection (EFI) ECUs: A significant revenue driver providing precise fuel delivery and emissions compliance for internal combustion engines.

Motor Control Units (MCUs): Intricate, high-value components for electric vehicles (EVs) developed by an in-house engineering team.

Genset Controllers: A modern segment catering to the growing demand for automated and efficient power generation solutions globally.

The operational presence serves an ecosystem of diverse global customers across a regional network, including significant manufacturing operations in Pune, Maharashtra, as of December 31, 2025.

The core operational strength is built around an engineering-first, innovation-led, and scalable manufacturing platform with a commitment to technical excellence. This strength is demonstrated by its internal research and development core, resulting in over 12 patents across regions and a dual-development approach that combines fundamental scientific research with rigorous automotive-grade validation.

Furthermore, the company has successfully expanded its footprint across international markets, maintaining a constant focus on reliability and quality through IATF and ISO certifications. As of December 31, 2025, the company has achieved significant scale with Rs 770.67 crore in nine-month revenue from operations.

The table below provides the segment-wise revenue contribution for the company for the nine months ended December 31, 2025:

Revenue Segment | Revenue Contribution (%) |

Mobility (2W, 3W, and EVs) | 84.63% |

Industrial (Generators and Others) | 15.37% |

The company identifies Prof. Shashikanth Suryanarayanan, Amit Arun Dixit, Manish Sharma, and Anaykumar Avinash Joshi as its promoters. The promoters collectively hold 22.26% of the pre-Offer paid-up equity share capital on a fully diluted basis. Key leadership includes Prof. Shashikanth Suryanarayanan (Managing Director), Amit Arun Dixit (Joint Managing Director), Manish Sharma (Whole-time Director and COO), and Rajesh Madhukar Sheth (Chief Financial Officer).

Industry Overview of SEDEMAC Mechatronics IPO

SEDEMAC Mechatronics Limited operates within the global and Indian control technologies industry, a significant pillar of the modern automotive and industrial economy, undergoing rapid technological transformation primarily driven by increasing regulatory mandates for emissions, a shift toward electrification, and the rising demand for fuel efficiency and user convenience.

The total market size for the domestic ISG ECU market in India was significant as of FY25, with SEDEMAC holding a leading around 35% market share by volume. Within the industrial sector, the Indian genset controller market is highly concentrated, with the company commanding an estimated 75% to 77% of the market share. Globally, the two-wheeler industry is projected to grow at a CAGR of 9% to 11% to reach 113 to 124 million units by 2030, while the electric two-wheeler segment is expected to clock much faster growth at a 17% to 19% CAGR.

Crucially, the segment remains a high-growth market for Tier-I suppliers capable of providing IP-backed, control-intensive solutions as OEMs move toward integrated electronics that provide competitive differentiation, particularly in high-growth segments like electric vehicle powertrains. This indicates massive untapped potential in the transition to sensorless motor control, the expansion of global export strategies, and the rising demand for cleaner, smarter industrial power equipment.

Within this intensely technical environment, the industry is navigating challenges such as the potential impact of semiconductor supply chain volatility, vulnerability to rapid shifts in battery technologies, and adapting to evolving global trade policies, including tariffs and local-content requirements in major export jurisdictions like the US and Europe.

Industry Statistics are sourced from the Omnitech Engineering Limited Red Herring Prospectus (RHP) dated February 18, 2026.

Financial Overview of SEDEMAC Mechatronics IPO

Particulars | Dec 31, 2025 (Rs Crores) | March 31, 2025 (Rs Crores) | March 31, 2024 (Rs Crores) | March 31, 2023 (Rs Crores) |

Revenue from Operations | 770.67 | 658.36 | 530.65 | 423.03 |

EBITDA Margin (%) | 20.90% | 19.00% | 15.66% | 12.82% |

Profit After Tax | 71.5 | 47.05 | 5.88 | 8.57 |

PAT Margin (%) | 9.28% | 7.15% | 1.11% | 2.03% |

Return on Equity (RoE) | 17.39% | 15.48% | 4.72% | 7.44% |

Return on Capital Employed (RoCE) | 32.52% | 33.79% | 28.87% | 17.51% |

Debt to Equity (Times) | 0.17 | 0.21 | 1.37 | 1.16 |

Note: RoE and RoCE figures for the period ended December 31, 2025, are for nine months and are not annualised.

Revenue from operations has shown robust growth, driven by the increasing adoption of ISG and EFI technologies by major OEMs. Revenue increased from Rs 423.03 crore in FY23 to Rs 530.65 crore in FY24, then accelerated to Rs 658.36 crore in FY25, indicating healthy growth momentum. This continued into the latest nine-month period, with revenue reaching Rs 770.67 crore for the period ending December 31, 2025.

In the EBITDA margin part, core business efficiency is seen through optimized manufacturing processes and high-value proprietary technology. The EBITDA margin stood at 12.82% in FY23, improved to 15.66% in FY24, and reached 19.00% in FY25. For the latest nine-month period ending December 31, 2025, the company reported an EBITDA margin of 20.90%, reflecting strong operating leverage as the business scales.

Profit After Tax (PAT) has demonstrated a significant upward trajectory, reflecting the company's successful commercialization of new technology platforms. PAT stood at Rs 8.57 crore in FY23, moderated to Rs 5.88 crore in FY24 due to one-time interest on CCPS, and reached a high of Rs 47.05 crore in FY25. For the latest nine-month period ending December 31, 2025, the company reported a PAT of Rs 71.50 crore.

The PAT margin highlights the company's improving bottom-line efficiency. The margin was 2.03% in FY23, dipping to 1.11% in FY24 before rebounding significantly to 7.15% in FY25. For the nine months ending December 31, 2025, the PAT margin stood at 9.28%, reflecting consistent growth and lower finance costs following the conversion of preference shares.

The Return on Equtiy (RoE) tracks the profitability relative to the equity base. The RoE showed a strong recovery, moving from 7.44% in FY23 to 15.48% in FY25. This trajectory correlates with the sharp rise in profitability and efficient capital utilization as the company's proprietary products achieve broader market adoption.

The Return on Capital Employed (RoCE) reflects how efficiently the company generates profits from its total capital. The RoCE improved from 17.51% in FY23 to 33.79% in FY25, highlighting a highly disciplined approach to deploying capital and maximizing returns on long-term investments.

The Debt to Equity ratio highlights the company's strengthening financial profile and reduced reliance on external borrowings. As of March 31, 2023, the ratio stood at 1.16 times, which significantly improved to 0.21 times as of March 31, 2025, and further to 0.17 times as of December 31, 2025. This demonstrates a highly conservative approach to leverage ahead of the SEDEMAC Mechatronics IPO date.

Financial figures are sourced from the Omnitech Engineering Limited Red Herring Prospectus (RHP) dated February 18, 2026 and are based on the period ending September 30, 2025.

Strengths and Risks of SEDEMAC Mechatronics IPO

Let's examine the strengths and weaknesses to determine if the SEDEMAC Mechatronics IPO is a good or bad investment for investors.

Strengths

First-to-Market Advantage and Patent Leadership: SEDEMAC was the first company in India to develop and manufacture sensorless commutation-based ISG ECUs. As of December 31, 2025, the company has supplied over 9.2 million such units, leveraging its 12 granted international patents to create high entry barriers for competitors.

Agility at Scale via Integrated Operations: The company possesses end-to-end control over design, engineering, and manufacturing. This allows for rapid innovation cycles and a swift response to customer-specific requirements, such as the ability to redesign products quickly during global semiconductor shortages to ensure uninterrupted OEM supply.

Synergy Across Mobility and Industrial Markets: SEDEMAC efficiently transfers proven technical solutions across segments. For example, its motor control architecture for 2W ISG systems has been successfully adapted for electric vehicle MCUs and power tool applications, allowing for consolidated procurement and significant economies of scale.

Quality Excellence and Trusted OEM Partnerships: The company has established long-term relationships with global market leaders like TVS Motor, Bajaj Auto, and Kirloskar Oil Engines. Its commitment to quality is reflected in consistently low part-failure rates and multiple platinum-level supplier awards for performance and reliability.

Highly Qualified Technical Nucleus: As of December 31, 2025, approximately 64.75% of the company's engineering team consists of graduates from premier Indian institutes like IITs, NITs, and BITS. This concentration of technical talent drives continuous innovation and maintains the company's status as a deep-tech leader.

Risks

High Customer Concentration: The company is highly vulnerable to client-specific risks, as it derived 75.48% of its revenue from operations from a single key customer, TVS Motor, during the nine-month period ended December 31, 2025. Loss of business from this client could severely impact financial stability.

Significant Segment Exposure: SEDEMAC is heavily dependent on the mobility segment, which contributed 84.63% of its revenue from operations in the nine months ended December 31, 2025. Any downturn or adverse regulatory shift in the two- and three-wheeler industry could materially harm its operations.

Dependence on Global Supply Chain for Critical Inputs: The company imports critical raw materials, including semiconductors and printed circuit boards, primarily from China. This exposes it to geopolitical risks, trade restrictions, and supply disruptions that could impact production costs and schedules.

Electrification and Technological Transition Risk: The rapid shift toward electric vehicles presents a risk to the company's ICE-focused product lines. While the company is expanding its EV portfolio, failure to achieve similar market relevance in the electric segment could lead to a decline in long-term revenue.

Geographic Concentration of Manufacturing: All current production requirements are met through two facilities located in Pune, Maharashtra. Any regional disruption, such as industrial accidents, local regulatory changes, or natural disasters, could adversely impact the company’s ability to meet customer commitments.

Strategies of SEDEMAC Mechatronics IPO

Expand Technologies Across Large Markets: A core pillar of the growth strategy is to deploy proprietary technology platforms into multiple large mobility and industrial markets, such as power tools and heavy-duty commercial vehicles. By targeting high-volume sectors, the company aims to achieve global relevance and broaden its revenue base.

Drive Technology and Product Differentiation: The company intends to maintain its leadership by continuously investing in differentiated, innovative control-intensive technologies. This includes developing rare-earth-free motors and advanced aftertreatment controllers to stay ahead of evolving emissions standards and end-user preferences.

Offer a Full Suite of Control-Intensive Products: SEDEMAC aims to increase its value per unit by offering a comprehensive suite of control-intensive products in every target segment. This multi-product approach deepens customer relationships and provides integrated solutions, such as combined ISG+EFI units that streamline vehicle electronics.

Establish and Sustain Partnerships with Market Leaders: The company prioritizes long-term, entrenched partnerships with leading Original Equipment Manufacturers (OEMs). By working with established, technically capable customers for early technology adoption, the firm reinforces its position as a respected and dependable solutions provider.

Leverage Synergies Across Markets, Products, and Supply Chains: The firm focuses on deploying shared technology platforms and common core architectures across its product portfolio. This strategy improves capital efficiency, drives cost reductions through consolidated procurement, and accelerates the time-to-market for new innovations.

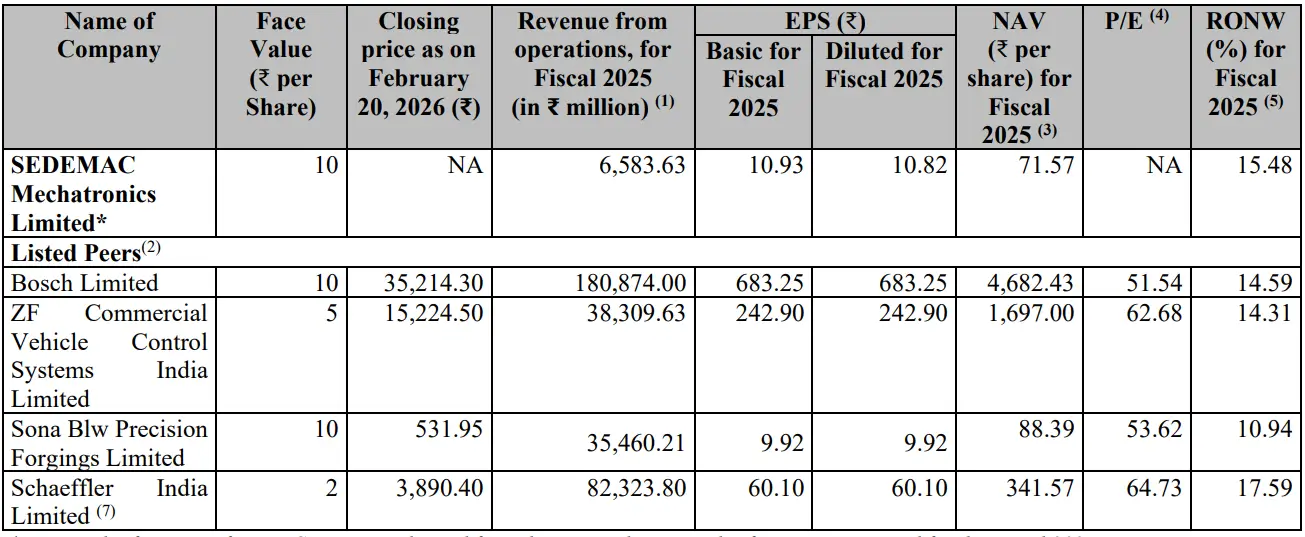

SEDEMAC Mechatronics IPO vs. Peers

SEDEMAC Mechatronics Limited reported revenue from operations of Rs 658.36 crore in FY25. On a restated basis, the company's revenue is lower compared to its established listed peer group, which includes Bosch Limited (Rs 18,087.40 crore), Schaeffler India Limited (Rs 8,232.38 crore (financial year ending on Dec 31)), ZF Commercial Vehicle Control Systems India Limited (Rs 3,830.96 crore) and Sona BLW Precision Forgings Limited (Rs 3,546.02 crore). This indicates that while SEDEMAC is a high-growth deep-tech player, its current scale is smaller compared to national and global market leaders.

In terms of operating profitability, the company's EBITDA margin for FY25 stood at 19.00%. This margin profile is competitive and sits higher than that of Bosch Limited (17.28%) and Schaeffler India Limited (18.99%), demonstrating SEDEMAC's strong edge in core operating efficiency derived from its proprietary, IP-heavy product offerings.

The Company is demonstrating healthy capital efficiency, reflected by a Return on Equity (RoE) of 22.01% in FY25. This RoE is notably higher than that reported by several peers, including Schaeffler India Limited (18.52%), Bosch Limited (15.58%), and Sona BLW Precision Forgings Limited (14.20%). This performance highlights the highly profitable and capital-efficient nature of SEDEMAC's design-led business model as it prepares for global expansion.

Objectives of SEDEMAC Mechatronics IPO

The offering consists of a total book-built issue worth around Rs 1,087 crore, which is comprised entirely of an Offer for Sale (OFS) of 80,43,300 equity shares. This IPO does not include a fresh issue component, which means 100% of the proceeds will be received by the selling shareholders.

The selling shareholders include Manish Sharma, Ashwini Amit Dixit, NRJN Family Trust, Xponentia Opportunities Fund II, Mace Private Limited, 360 One Special Opportunities Fund – Series 8, 360 One Monopolistic Market Intermediaries Fund, HDFC Life Insurance Company Limited and Xponentia Opportunities Limited.

SEDEMAC Mechatronics IPO Details

IPO Dates

SEDEMAC Mechatronics IPO will be open for subscription from March 04, 2026, to March 06, 2026. The allotment of shares to investors will take place on March 09, 2026, and the company is expected to be listed on the NSE and BSE on March 11, 2026.

IPO Issue Price

SEDEMAC Mechatronics is offering its shares in the price band of Rs 1,287 to Rs 1,352 per share. This means you would require an investment of Rs. 14,872 per lot (11 shares) if you are bidding for the IPO at the upper price band.

IPO Size

SEDEMAC Mechatronics is offering a total offer for sale of 80,43,300 shares amounting to Rs 1,087 crore, to be received by the selling shareholders in the IPO.

IPO Allotment Status

Investors who applied for the IPO can check their IPO allotment status on March 09, 2026, through the registrar's website, MUFG Intime India Private Limited, BSE, NSE, or through the stockbroker platform.

IPO Listing Date

The shares of SEDEMAC Mechatronics are expected to be listed on the NSE and BSE on March 11, 2026.

IPO Application Link

Open demat account with Rupeezy today and enjoy a seamless experience when applying for the IPO. With an easy-to-use platform, Rupeezy makes the IPO application process quick and hassle-free.

Apply for SEDEMAC Mechatronics IPO

Important IPO Details | |

Bidding Date | March 04, 2026 to March 06, 2026 |

Allotment Date | March 09, 2026 |

Listing Date | March 11, 2026 |

Issue Price | Rs 1,287 to Rs 1,352 per share |

Lot Size | 11 Shares |

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

All Category