Is Sai Parenteral's IPO Good or Bad – Detailed Review

00:00 / 00:00

Summary:

| ||

Sai Parenteral's Limited’s IPO is set to open its initial public offering from March 24, 2026, to March 27, 2026. When considering applying for this IPO, potential investors might have questions about whether Sai Parenteral's IPO is a good investment and if it's worth subscribing to.

This article provides a comprehensive analysis of Sai Parenteral's IPO, covering its business operations and fundamental analysis from its RHP to help you make an informed investment decision.

Investments in the securities market are subject to market risks. Read all the related documents carefully before investing.

Sai Parenteral's IPO Review

Sai Parenteral's Limited IPO is open for subscription from March 24, 2026, to March 27, 2026, with listing expected on April 2, 2026, on NSE and BSE.

The company is a diversified pharmaceutical formulations player with capabilities in research, development, and manufacturing. It operates in the business of Branded Generic Formulations and Contract Development and Manufacturing Organisation (CDMO) products and services for both domestic and international markets. As of Fiscal 2025, the company reported revenue from operations of Rs 1,58.50 crore, driven by its robust portfolio across therapeutic areas like cardiovascular, neuropsychiatry, anti-diabetic, and antibiotics.

Sai Parenteral's operates through five manufacturing facilities, with four located in Hyderabad (Telangana) and one in Ongole (Andhra Pradesh). The company offers a wide array of dosage forms, including injectables, tablets, capsules, liquid orals, and ointments. Promoted by Anil Kumar Karusala, Vijitha Gorrepati, and Karusala Aruna, the promoters hold a 55.81% pre-offer stake in the company.

The company operates in the rapidly expanding Indian pharmaceutical market, which is the world's third-largest by volume. With the drug formulation market projected to reach $109 billion by 2033, Sai Parenteral's is strategically positioned to capitalize on this growth. Furthermore, the company recently completed a transformative acquisition of a 74.64% stake in Noumed Pharmaceuticals Pty Limited (Australia), marking its entry into high-value regulated markets.

Financially, Sai Parenteral's shows steady growth and consistent profitability. Revenue from operations reached Rs 1,631.06 crore in FY25, with Rs 869.18 crore reported for the six months ended September 30, 2025. Restated Profit After Tax (PAT) for FY25 stood at Rs 144.54 crore, showing a significant increase from Rs 84.15 crore in FY24.

The company maintains healthy operational metrics, with an EBITDA margin of 24.18% in FY25 and a Return on Equity (RoE) of 15.09%. Sai Parenteral's intends to utilize the IPO proceeds to fund capacity expansion, upgrade its manufacturing facilities to EU-GMP/PIC/S standards, and establish a new R&D centre.

Key strengths include its diversified product portfolio, strategically located and accredited manufacturing facilities, and a track record of value-accretive acquisitions. Primary risks include geographical concentration of facilities in Southern India, high dependence on the injectables segment, and exposure to complex international regulatory environments.

The book-built issue consists of a Fresh Issue of up to Rs 285 crore and an Offer for Sale (OFS) of up to Rs 124 crore received by the Investor Selling Shareholders.

Shares are priced between Rs 372 and Rs 392 per share, with a minimum lot size of 38 shares.

What does Sai Parenteral's do?

Sai Parenteral's Limited is a Hyderabad-based pharmaceutical company that provides a comprehensive spectrum of formulation services. Originally incorporated in 2001, the company has evolved from a parenteral specialist to a diversified player providing end-to-end CDMO solutions and branded generics, ensuring that patients globally have access to high-quality medicinal products.

The company handles the entire life cycle of pharmaceutical solutions, from in-house formulation research and development (FR&D) to the preparation of regulatory dossiers and large-scale commercial manufacturing. They have sterile manufacturing capabilities for critical care and antibiotics delivered through dry powder injections, pre-filled syringes, ampoules, and vials.

Sai Parenteral's Business Segments

Sai Parenteral's serves major industrial players and state utilities through two main categories:

Branded Generic Formulations: This involves producing off-patent products sold under the company's own brands. It includes domestic sales to government agencies and private sector super stockists, as well as exports to markets like Australia, the Philippines, and South Africa. This segment accounted for 80.29% of net revenue in FY25.

CDMO Products and Services: The company provides comprehensive drug development and manufacturing services for multinational pharmaceutical companies. This segment accounted for 19.71% of net revenue in FY25 and is growing rapidly.

Key Operational Features

The company’s operations are supported by an established distribution network in India and strategic partnerships with 7 international distributors. To maintain high standards, they operate TGA-Australia (Therapeutic Goods Administration) and WHO-GMP accredited facilities. They are also pioneering new delivery formats like lyophilized vials and cartridges through their proposed capacity expansion.

The company is led by Managing Director Anil Kumar Karusala, who brings over 31 years of industry experience, supported by a professional management team with deep expertise in regulatory affairs and pharmaceutical engineering.

What is the market opportunity for Sai Parenteral's?

Sai Parenteral's is riding a wave in the global and Indian pharmaceutical industry. The Indian drug formulation market is currently valued around USD 47 billion in 2025 which is projected to grow at a CAGR of 11.2% to reach USD 109 billion by 2033. As chronic disease prevalence increases and healthcare access improves, the demand for affordable generics and specialized injectables expands.

The global CDMO market represents a massive opportunity, projected to reach USD 609 billion by 2033 from the current USD 297 billion in 2025. By upgrading facilities to EU-GMP standards and leveraging the recent acquisition of Noumed's 451 approved dossiers, Sai Parenteral's is poised to capture a larger share of the regulated export market.

Industry Statistics are sourced from the Marketysers Industry Report dated September 2025, included in the Sai Parenteral's Limited Red Herring Prospectus.

Is Sai Parenteral's Limited Profitable?

Particulars | Sept 30, 2025 (Rs Cr) | FY 2025 (Rs Cr) | FY 2024 (Rs Cr) | FY 2023 (Rs Cr) |

Revenue from Operations | 869.18 | 1,631.06 | 1,537.61 | 967.96 |

EBITDA Margin (%) | 18.68% | 24.18% | 20.62% | 18.22% |

Profit After Tax | 77.64 | 144.54 | 84.15 | 43.76 |

PAT Margin (%) | 8.93% | 8.88% | 5.47% | 4.52% |

Return on Equity (RoE) | 5.09% | 15.09% | 11.01% | 13.90% |

Return on Cap. Employed (RoCE) | 9.28% | 28.92% | 20.52% | 21.04% |

Fixed Asset Turnover | 2.02 | 3.76 | 2.56 | 2.22 |

Note: Not annualized for the 6-month period.

Revenue from operations grew from Rs 967.96 crore in FY23 to Rs 1,631.06 crore in FY25, a significant expansion driven by CDMO scaling and the integration of Revat Laboratories. Domestic branded generics maintained strong momentum, while the CDMO vertical achieved an exceptional 80.46% CAGR over the three-year period.

Operational efficiency reached new heights with EBITDA margins increasing to 24.18% in FY25, up from 18.22% in FY23. This margin expansion reflects a deliberate strategic pivot toward high-value regulated market export formulations and enhanced operating leverage across its five manufacturing units.

Restated Profit After Tax (PAT) rose from Rs 43.76 crore in FY23 to Rs 144.54 crore in FY25, highlighting consistent profitability. Shareholder value remained robust with a Return on Equity (RoE) of 15.09% in FY25, demonstrating effective equity utilization.

The Return on Capital Employed (RoCE) also improved to 28.92% in FY25, reflecting efficient use of debt and equity to drive earnings. Furthermore, the Fixed Asset Turnover ratio reached 3.76 in FY25, indicating high productivity from the company’s manufacturing base.

Financial figures are sourced from the Sai Parenteral's Red Herring Prospectus (RHP) dated March 16, 2026.

Strengths and Risks of Sai Parenteral's IPO

Let's examine the strengths and weaknesses to determine whether Sai Parenteral's IPO is good or bad for investors.

Strengths

Diversified Product Portfolio: Capabilities across various therapeutic areas and multiple dosage forms including high-growth injectables.

Accredited Manufacturing Base: Facilities hold prestigious certifications like TGA-Australia and WHO-GMP, with upcoming EU-GMP alignment.

Strategic Global Footprint: Recent acquisition of Noumed provides a direct platform for expansion in the Australia and New Zealand markets.

Strong CDMO Focus: Rapidly growing vertical with long-term contracts and an expanding library of in-house developed dossiers.

Experienced Leadership: Led by promoters with over three decades of institutional knowledge in the pharmaceutical domain.

Risks

Geographic Concentration: All Indian manufacturing facilities are located in Telangana and Andhra Pradesh, exposing them to regional risks.

Dependence on Injectables: A significant portion of revenue is derived from the injectables segment; any demand drop here would impact financials.

Regulatory Scrutiny: The industry is subject to extensive periodic inspections; any adverse findings can lead to product recalls or license suspensions.

Raw Material Volatility: Dependence on a diversified supplier base without long-term contracts for critical APIs and excipients.

Integration Risks: Challenges associated with managing and integrating the newly acquired Australian operations (Noumed).

Strategies of Sai Parenteral's IPO

Expanding global injectable market presence: Upgrading Unit I and Unit II to meet EU-GMP and PIC/S standards to facilitate exports to high-margin markets like the European Union and Latin America.

Scaling CDMO through R&D and manufacturing: Transitioning to an integrated service model by upgrading Units III and IV and leveraging the new R&D centre to offer end-to-end development for multinational clients.

Developing sovereign manufacturing in Australia: Building the Adelaide facility through Noumed to establish local production, improve supply chain resilience, and capture margins by reducing international logistics costs.

Innovating via new product development: Aiming to file 60 new dossiers by Fiscal 2028 and commercializing 451 acquired TGA dossiers, focusing on complex generics and upcoming patent expirations.

Growing international branded generic sales: Utilizing Noumed’s dossier library to expand the "Sai Parenterals" brand across Asia and Africa, specifically targeting PIC/S and Semi-Regulated Markets.

Pursuing value-accretive strategic acquisitions: Continuing a disciplined approach to inorganic growth to acquire new technologies, regulatory dossiers, or manufacturing capacities that complement the existing portfolio.

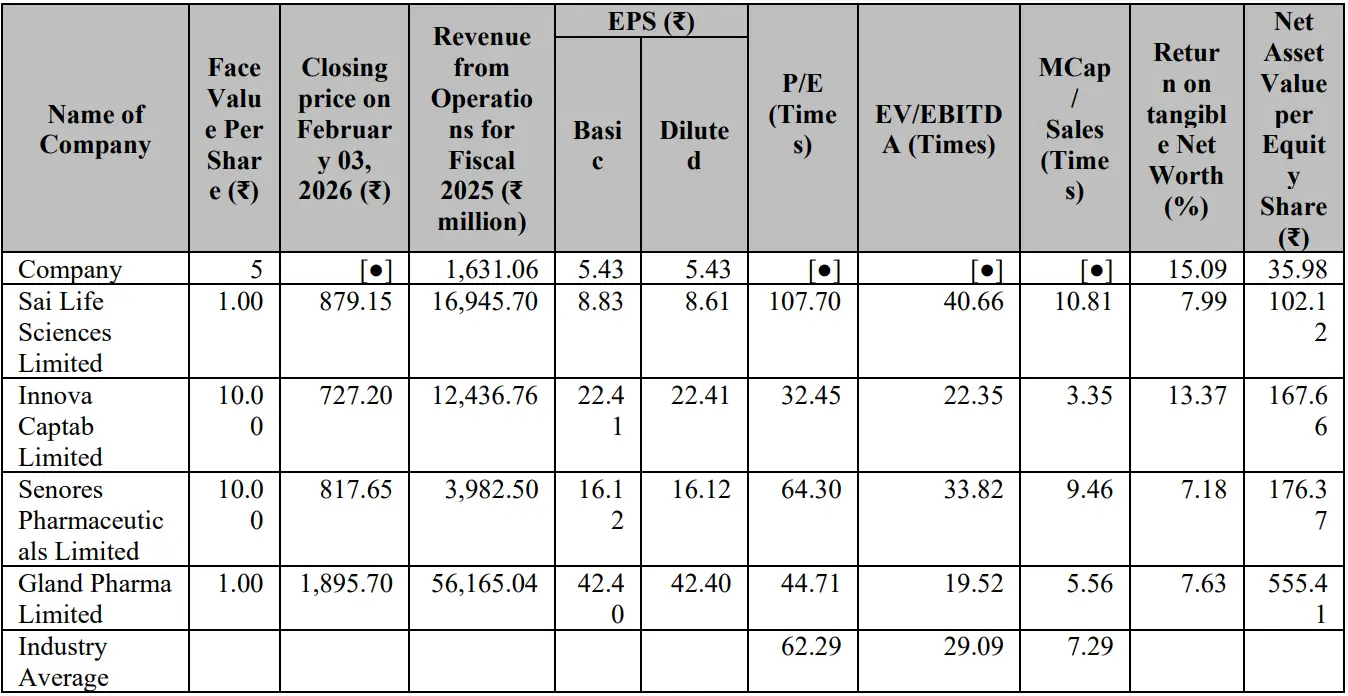

Sai Parenteral's IPO vs. Peers

The following securities are mentioned as examples for comparative purposes only and do not constitute a recommendation to buy or sell.

Sai Parental's Limited demonstrates financial metrics that compare favorably with its listed industry peers.

Efficiency and Profitability: Sai Parental's achieves an EBITDA margin of 24.18% in FY25, placing it higher than Innova Captab Limited (15.94%) and closely following specialized players like Gland Pharma Limited (26.40%).

Shareholder Returns: The company's Return on Equity (RoE) of 15.09% significantly outperforms the industry high seen in Sai Life Sciences Limited (7.99%), Innova Captab Limited (13.37%), Senores Pharmaceuticals Limited (7.18%), and Gland Pharma Limited (7.63%).

Asset Utilization: With a Fixed Asset Turnover of 3.76, Sai Parental's shows greater productivity per unit of manufacturing infrastructure compared to Innova Captab Limited (1.62) and Senores Pharmaceuticals Limited (2.10).

Capital Deployment: A Return on Capital Employed (RoCE) of 28.92% in FY25 indicates a more efficient generation of earnings from its total capital base compared to Sai Life Sciences Limited (12.52%) and Gland Pharma Limited (14.91%).

Objectives of Sai Parenteral's IPO

The offering consists of a total book-built issue comprising a Fresh Issue of Rs 285 crore and an Offer for Sale of Rs 124 crore, which the Selling Shareholders will receive in this IPO.

The company will use the proceeds primarily for:

Scaling and modernizing production capacities: Rs 110.80 crore.

Founding a dedicated research and development centre: Rs 18.02 crore.

Prepaying or repaying outstanding company borrowings: Rs 14.30 crore.

Meeting immediate and future working capital demands: Rs 33.00 crore.

Settling acquisition-linked loans for the Noumed Australia transaction: Rs 35.64 crore.

General Corporate Purposes: Rs 73.24 crore.

Sai Parenteral's IPO Details

IPO Dates

Sai Parenteral's IPO will be open for subscription from March 24, 2026, to March 27, 2026. The allotment of shares to investors will take place on March 30, 2026, and the company is expected to be listed on the NSE and BSE on April 2, 2026.

IPO Issue Price

Sai Parenteral's is offering its shares in the price band of Rs 372 to Rs 392 per share. This means you would require an investment of Rs 14,896 per lot (38 shares) if you are bidding for the IPO at the upper price band.

IPO Size

Sai Parenteral's is launching an IPO consisting of a mix of Fresh Issue and Offer for Sale (OFS) totalling 1.04 crore shares. The total value of the issue is valued at Rs 409 crore.

IPO Allotment Status

Investors who applied for the IPO can check their IPO allotment status on March 30, 2026, through the registrar's website, Bigshare Services Private Limited, BSE, NSE, or through their stockbroker platform.

IPO Listing Date

The shares of Sai Parenteral's are expected to be listed on the NSE and BSE on April 2, 2026.

IPO Application Link

Open demat account with Rupeezy today and enjoy a seamless experience when applying for the IPO. With an easy-to-use platform, Rupeezy makes the IPO application process quick and hassle-free.

Apply for Sai Parenteral's IPO

Important IPO Details | |

Bidding Date | March 24, 2026 to March 27, 2026 |

Allotment Date | March 30, 2026 |

Listing Date | April 2, 2026 |

Issue Price | Rs 372 to Rs 392 per share |

Lot Size | 38 Shares |

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

Disclaimer

Investments in the securities market are subject to market risks. Read all the related documents carefully before investing. Rupeezy (SEBI RA Registration: INH000013332) provides this content for informational purposes; any securities quoted are for educational display and not as a recommendation. All charts and graphs are based on independent research and reliable sources for the period mentioned within the specific data set. Sometimes we take graphs from external sources. This communication does not promise or assure any fixed, guaranteed, or indicative returns to any client. For our complete registered office address, Member ID, and full SEBI registration details, please refer to our official website.

All Category