Is Om Power Transmission IPO Good or Bad – Detailed Review

00:00 / 00:00

Summary:

| ||

Om Power Transmission Limited’s IPO is set to open its initial public offering from April 09, 2026, to April 13, 2026. When considering applying for this IPO, potential investors might have questions about whether Om Power Transmission IPO is a good investment and if it's worth subscribing to.

This article provides a comprehensive analysis of Om Power Transmission's IPO, covering its business operations and a fundamental analysis of its RHP to help you make an informed investment decision.

Investments in the securities market are subject to market risks. Read all the related documents carefully before investing.

Om Power Transmission IPO Review

Om Power Transmission Limited IPO is open for subscription from April 09, 2026, to April 13, 2026, with listing expected on April 17, 2026, on NSE and BSE.

The company is a specialized Engineering, Procurement, and Construction (EPC) player in the power transmission infrastructure sector. It provides end-to-end services, including design, engineering, supply, installation, and commissioning of high-voltage (HV) and extra-high-voltage (EHV) transmission lines and substations. As of the nine months ended December 31, 2025, the company reported revenue from operations of Rs 274.54 crore, driven by its strong capabilities in executing complex infrastructure projects for state utilities and private players.

Om Power Transmission operates primarily out of Ahmedabad, Gujarat, and has established itself as a "Class AA" contractor with GETCO. The company handles projects ranging from 11kV to 400kV. Promoted by Kalpesh Dhanjibhai Patel, Kanubhai Patel, and Vasantkumar Narayanbhai Patel, the promoters maintain significant institutional knowledge with over 30 years of experience each in the electrical sector.

The company operates in the expanding Indian power T&D (Transmission and Distribution) market. With the government's focus on renewable energy zones and the Revamped Distribution Sector Scheme (RDSS), Om Power Transmission is strategically positioned to capitalize on the massive grid expansion required for green energy evacuation. Recently, the company has successfully expanded its footprint into North India, securing projects in Punjab and Rajasthan.

Financially, Om Power Transmission shows rapid growth and robust profitability. Revenue from operations grew at a CAGR of 52.45% between FY23 and FY25. For the nine months ended December 31, 2025, it reported a Profit After Tax (PAT) of Rs 23.36 crore, already exceeding the full-year PAT of FY25 (Rs 22.08 crore).

The company maintains healthy operational metrics, with an EBITDA of Rs 34.24 crore in the first nine months of FY26 and a Return on Equity (RoE) of 24.28%. Om Power Transmission intends to utilize the IPO proceeds to fund the purchase of specialized machinery, repay existing debt, and meet its long-term working capital requirements.

Key strengths include its "Class AA" accreditation, a diversified order book worth Rs 744.60 crore, and a track record of completing complex projects like utility shifting for the high-speed bullet train corridor. Primary risks include regional concentration in Gujarat, high dependency on public sector undertakings (PSUs), and the working-capital-intensive nature of the EPC business.

The book-built issue consists of a Fresh Issue of up to 75,75,000 shares and an Offer for Sale (OFS) of up to 10,00,000 shares offered by the Promoter Selling Shareholders.

Shares are priced between Rs 166 and Rs 175 per share, with a minimum lot size of 85 shares.

What does Om Power Transmission do?

Om Power Transmission Limited is an Ahmedabad-based infrastructure company that provides a comprehensive spectrum of power transmission services. Originally incorporated in 2011, the company has evolved from a regional contractor to a diversified EPC player providing solutions for substations, underground cabling, and overhead transmission lines.

The company handles the entire life cycle of power infrastructure, from detailed route surveys and design to the erection of massive 400kV towers and stringing of conductors. They also provide vital Operation and Maintenance (O&M) services, currently maintaining around 124 substations to ensure grid reliability.

Om Power Transmission, a Class AA contractor, commands a strong presence in the high-voltage segment, leveraging an order book that grew to Rs 744.60 crore as of December 2025.

Om Power Transmission Business Segments

Om Power Transmission serves state utilities and private industrial players through four main categories:

Transmission Line EPC Projects: This involves the construction of overhead lines up to 400kV. This segment is the largest contributor to the company's order book with Rs 518.89 crore.

Substation EPC Projects: Building and commissioning high-voltage substations (up to 220kV), including civil works and SCADA integration.

Underground Cabling: Laying high-voltage and extra-high-voltage cables in urban environments where overhead lines are not feasible.

Operation & Maintenance (O&M): Providing 24/7 maintenance services for existing power assets to ensure zero downtime.

Key Operational Features

The company’s operations are supported by a large fleet of specialized equipment, including digital pullers, tensioners, and articulated cranes. They hold ISO certifications, highlighting safety and quality. Managing Director Kanubhai Patel and Chairman Kalpesh Dhanjibhai Patel lead the company, leveraging their combined decades of expertise in electronic and power transmission projects.

What is the market opportunity for Om Power Transmission?

Om Power Transmission Limited operates within the Indian power transmission and distribution (T&D) infrastructure industry, a cornerstone of the modern energy economy. The sector is undergoing rapid transformation, driven by ambitious renewable energy integration targets and the government’s push for a synchronized "One Nation, One Grid" architecture.

The total addressable market for India’s power transmission and distribution sector is projected to reach a significant valuation by 2030, with a planned capex of Rs 9.15 lakh crore between FY23 and FY32.

Nationally, the government aims to add approximately 76,787 circuit kilometers of transmission lines by 2032, highlighting a massive runway for EHV-certified EPC players.

Crucially, the segment remains a high-growth market as utilities transition toward automated, SCADA-integrated (Supervisory Control and Data Acquisition) substations and underground cabling to manage urban grid reliability and evacuate 500 GW of non-fossil fuel power by 2030.

Despite this potential, the industry faces persistent challenges, including land acquisition delays, raw material price volatility, and the high working capital intensity required to sustain a competitive L1 bidding environment.

Industry Statistics are sourced from the Om Power Transmission Limited Red Herring Prospectus (RHP) dated April 04, 2026.

Is Om Power Transmission Limited Profitable?

Particulars | Dec 31, 2025 (Rs Cr) | FY 2025 (Rs Cr) | FY 2024 (Rs Cr) | FY 2023 (Rs Cr) |

Revenue from Operations | 274.54 | 279.44 | 182.76 | 120.24 |

EBITDA Margin (%) | 12.38% | 12.66% | 7.85% | 9.80% |

Profit After Tax | 23.37 | 22.08 | 7.41 | 6.24 |

PAT Margin (%) | 8.45% | 7.84% | 4.02% | 5.12% |

Return on Equity (RoE) | 24.28% | 35.83% | 15.77% | 15.18% |

Return on Capital Employed (RoCE) | 26.53% | 41.76% | 18.41% | 15.45% |

Debt to Equity Ratio | 0.32 | 0.26 | 0.52 | 0.59 |

Note: The figures for the period ended Dec 31, 2025, are for 9 months and are not annualized.

Revenue from operations has shown robust growth, more than doubling from Rs 120.23 crore in FY23 to Rs 279.43 crore in FY25, indicating strong demand for power infrastructure. Core business efficiency remained healthy, with EBITDA margins improving from 9.80% in FY23 to 12.66% in FY25 as the company scaled its operations.

Profit After Tax (PAT) demonstrated a significant upward trajectory, rising from Rs 6.23 crore in FY23 to Rs 22.08 crore in FY25. This bottom-line growth is reflected in the PAT margin, which expanded from 5.12% to 7.84% over the same period.

The company's capital efficiency improved remarkably, with Return on Equity (RoE) jumping from 15.18% in FY23 to 35.83% in FY25. Similarly, Return on Capital Employed (RoCE) grew from 15.45% to 41.76%, showcasing highly efficient utilization of its capital base.

The Debt-to-Equity ratio strengthened significantly, reducing from 0.59 times in FY23 to 0.26 times in FY25, highlighting a much more conservative financial profile ahead of the IPO.

Financial figures are sourced from the Om Power Transmission Limited Red Herring Prospectus (RHP) dated April 04, 2026.

Strengths and Risks of Om Power Transmission IPO

Let's examine the strengths and weaknesses to determine whether the Om Power Transmission IPO is good or bad for investors.

Strengths

Proven Execution and Timely Completion Record: The company has over 14 years of experience, having commissioned over 1,000 circuit kilometers (CKM) of transmission lines and 11 substations since 2011. Notable achievements include the completion of complex projects ahead of schedule, such as a 66 kV line for a major automobile client in 4 months and an 83 km line for GETCO.

High-Voltage Technical Accreditation: Registered as a Class ‘AA’ contractor with the Gujarat Energy Transmission Corporation Limited (GETCO), the company is authorized to handle massive 400 kV transmission lines and 220 kV substation projects, representing a high entry barrier in the EHV (Extra High Voltage) segment.

Robust and Diversified Order Book: As of December 31, 2025, the company maintains an unexecuted order book of Rs 744.60 crore across multiple verticals, including transmission lines, substations, and underground cabling, providing strong revenue visibility for the next 24 months.

Strong and Consistent Financial Growth: The company demonstrated exceptional scalability, with revenue CAGR of 52.45% and PAT CAGR of 88.17% between FY23 and FY25. For 9M FY26, the PAT reached Rs 23.36 crore, already surpassing the previous full year's earnings.

Experienced Leadership and Domain Expertise: Led by promoters Kalpesh Patel, Kanubhai Patel, and Vasantkumar Patel, who each bring over 31 years of institutional knowledge in power infrastructure, enabling the company to maintain deep-rooted relationships with state utilities and manage complex regulatory landscapes.

Risks

Significant Customer Concentration: The company is highly dependent on a few key clients, with GETCO alone contributing 71.55% of revenue from operations for the nine-month period ended December 31, 2025. Any loss of business or delay in payments from this client could severely impact financial stability.

Competitive Bidding and Pricing Pressure: Most projects are secured through a competitive "L1" (lowest bidder) process. Aggressive bidding by competitors can compress profit margins, and any failure to accurately estimate project costs could lead to significant financial losses.

High Working Capital Intensity: The EPC business model requires substantial bank guarantees and performance bonds. As of December 31, 2025, the company had outstanding bank guarantees worth Rs 127.04 crore, reflecting high capital needs to sustain and bid for new projects.

Regional Concentration Risk: Historically, 100% of the company's completed projects were located in Gujarat. While expanding into other states, any adverse social, political, or economic shifts within Gujarat could still materially harm its overall operations.

Dependency on Public Sector Undertakings (PSUs): Approximately 83.74% of the current Order Book consists of projects with PSUs. These contracts are subject to complex government internal processes, policy changes, and budgetary allocations, which could lead to project delays or cancellations.

Strategies of Om Power Transmission IPO

Geographic Expansion Beyond Gujarat: A core growth strategy is to diversify the company's revenue base by moving into North India. It has already secured initial projects in Punjab and Rajasthan to tap into national renewable energy corridors and reduce regional dependency.

Operational Efficiency via Specialized Asset Ownership: The company intends to utilize part of the IPO proceeds (Rs 11.21 crore) to purchase advanced machinery like Digital Pullers and Tensioners. This self-reliance on heavy equipment aims to reduce hiring costs and accelerate the stringing and commissioning of EHV projects.

Strategic Debt Management for Financial Flexibility: The company plans to deploy Rs 25.00 crore to repay or prepay existing bank borrowings. This strategy is designed to improve the debt-to-equity ratio, reduce finance costs, and enhance its ability to leverage the balance sheet for larger future contract bids.

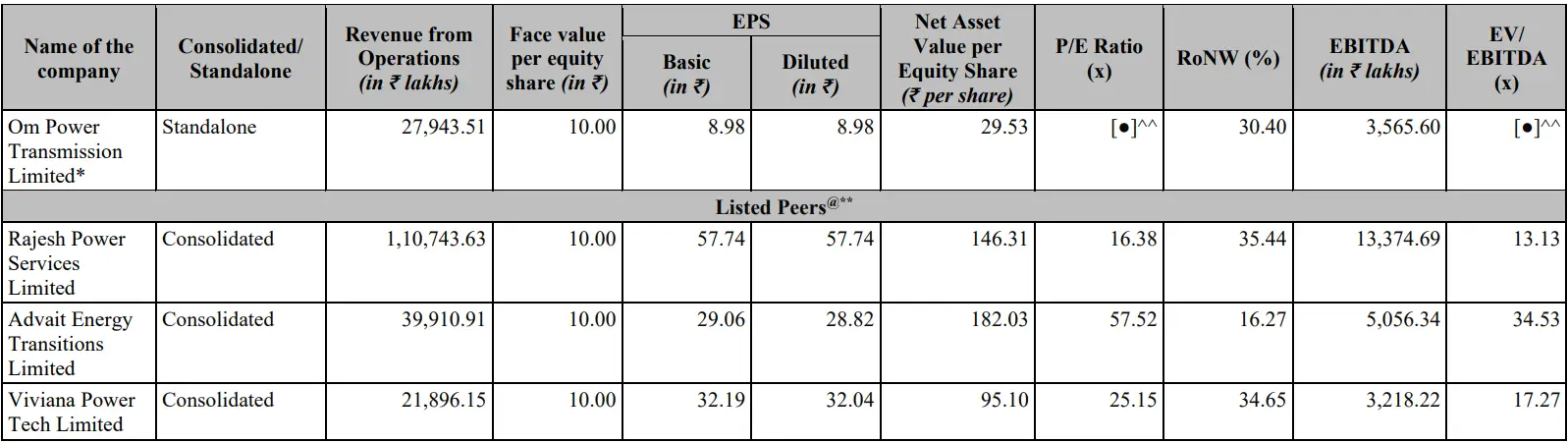

Om Power Transmission IPO vs. Peers

Om Power Transmission Limited demonstrates financial metrics that compare favorably with its listed industry peers.

Efficiency and Profitability: Om Power Transmission achieves an EBITDA margin of 12.66% in FY25, placing it competitively alongside Rajesh Power Services Limited (12.1%) and Viviana Power Tech Limited (14.66%).

Shareholder Returns: The company's Return on Equity (RoE) of 35.83% in FY25 significantly outperforms industry peers such as Advait Energy Transitions Limited (23.71%) and highlights exceptional value generation for its shareholders.

Asset Utilization: With a Net Capital Turnover Ratio of 4.57 in FY25, Om Power Transmission shows greater productivity per unit of working capital compared to specialized players like Advait Energy Transitions Limited (3.06).

Capital Deployment: A Return on Capital Employed (RoCE) of 41.76% in FY25 shows that the company is better at making money from its total capital compared to Advait Energy Transitions Limited (25.38%) and is on par with the high-efficiency levels of Viviana Power Tech.

Objectives of Om Power Transmission IPO

The offering consists of a total book-built issue, which includes a Fresh Issue of Rs 133 crore and an Offer for Sale of Rs 18 crore, with the Selling Shareholders receiving the proceeds in this IPO.

The company will primarily use the proceeds from the fresh issue for:

Funding Capital Expenditure for the purchase of machinery and equipment: Rs 11.20 crore.

Prepaying or repaying outstanding company borrowings: Rs 25 crore.

Meeting immediate and future working capital demands: Rs 55 crore.

General Corporate Purposes: Rs 41.79 crore.

Om Power Transmission IPO Details

IPO Dates

Om Power Transmission IPO will be open for subscription from April 09, 2026, to April 13, 2026. The allotment of shares to investors will take place on April 15, 2026, and the company is expected to be listed on the NSE and BSE on April 17, 2026.

IPO Issue Price

Om Power Transmission is offering its shares in the price band of Rs 166 to Rs 175 per share. This means you would require an investment of Rs 14,875 per lot (85 shares) if you are bidding for the IPO at the upper price band.

IPO Size

Om Power Transmission is launching an IPO consisting of a mix of fresh issues and offers for sale (OFS) totalling 85.75 lakh shares. The total value of the issue is worth Rs 150 crore.

IPO Allotment Status

Investors who applied for the IPO can check their IPO allotment status on April 15, 2026, through the registrar's website, MUFG Intime India Private Limited, BSE, NSE, or through their stockbroker platform.

IPO Listing Date

The shares of Om Power Transmission are expected to be listed on the NSE and BSE on April 17, 2026.

IPO Application Link

Open demat account with Rupeezy today and enjoy a seamless experience when applying for the IPO. With an easy-to-use platform, Rupeezy makes the IPO application process quick and hassle-free.

Apply for Om Power Transmission IPO

Important IPO Details | |

Bidding Date | April 09, 2026 to April 13, 2026 |

Allotment Date | April 15, 2026 |

Listing Date | April 17, 2026 |

Issue Price | Rs 166 to Rs 175 per share |

Lot Size | 85 Shares |

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

Disclaimer

Investments in the securities market are subject to market risks. Read all the related documents carefully before investing. Rupeezy (SEBI RA Registration: INH000013332) provides this content for informational purposes; any securities quoted are for educational display and not as a recommendation. All charts and graphs are based on independent research and reliable sources for the period mentioned within the specific data set. Sometimes we take graphs from external sources. This communication does not promise or assure any fixed, guaranteed, or indicative returns to any client. For our complete registered office address, Member ID, and full SEBI registration details, please refer to our official website.

All Category