Can Mutual Funds Make You Rich? A Practical Wealth Plan

00:00 / 00:00

In today’s world, building massive wealth is something almost everyone aspires to. And for many, especially salaried individuals, mutual funds are seen as a practical path to achieve it. But despite their popularity, many investors, especially beginners, often find themselves asking one question: "Can mutual funds make you rich over time?"

You might be a bit disappointed, but the answer to whether mutual funds can fully make you rich isn’t a simple one. It’s not entirely a yes, and it’s not a clear no either.

To understand why the answer isn’t a clear yes or no, we need to look at how your desired wealth is actually created through mutual funds. So let’s walk through the process step by step.

The Process of Wealth Creation in Mutual Funds

Now that we’ve set the context, let’s break down how wealth is actually built through mutual funds.

1. Define Your Wealth Number

Once you decide to build wealth, the first step is to define what “wealth” actually means to you. There is no single number that fits everyone. It varies from person to person based on their goals, lifestyle, and priorities.

For some, it could mean buying a house, for others it might be planning for retirement, funding a child’s education, or achieving financial independence. The purpose behind your goal plays a big role in shaping your target.

The clearer you are about why you’re building this wealth, the easier it becomes to figure out how much you will actually need.

2. Decide Your Timeline

Every goal needs a timeline, and in your wealth creation journey through mutual funds, this is something you define for yourself. The timeline simply refers to the number of years within which you want to achieve your target.

This plays an important role in shaping your investment plan, as it helps determine how much you need to invest regularly to reach your goal.

At the same time, time is one of the biggest advantages you have. The longer you stay invested, the more you benefit from compounding, where your returns get reinvested and start generating returns of their own.

In the early stages of investing, especially in equity-oriented mutual funds, you may experience periods of volatility and fluctuations in returns.

However, over longer investment horizons, these short-term market movements generally tend to even out, allowing compounding and long-term market growth to work more effectively in your favour. This is why a longer timeline can significantly improve your overall wealth creation.

To understand the impact of time, consider these two SIP scenarios with an assumed return of 10% per annum (As per AMFIs Best Practices Guidelines):

Scenario | Monthly SIP | Investment Period | Total Invested | Approx. Final Corpus |

Scenario 1 | Rs.5,000 | 20 Years | Rs.12 Lakhs | Rs.38.28 Lakhs |

Scenario 2 | Rs.10,000 | 10 Years | Rs.12 Lakhs | Rs.20.65 Lakhs |

Even though both investors put in the same total amount of Rs.12 Lakhs, the investor who stayed invested for longer ends up building a significantly larger corpus. This highlights the true power of time and compounding in mutual fund investing.

3. Account for Inflation

Inflation is one of the biggest threats to your wealth, and ignoring it is one of the most common mistakes people make in their wealth creation journey. Over time, inflation gradually reduces the purchasing power of your money, meaning the same amount will buy you far less in the future than it does today.

This is why it is important to account for inflation while planning your investments. Your target amount should not just reflect what you need today, but what that goal will actually cost in the future.

Adjusting your goal amount for inflation helps you arrive at an inflation-adjusted target and gives you a clearer picture of how much you need to invest to realistically achieve your financial goal.

Say your goal is to achieve Rs.1 Crore after 20 years, and let us assume the average inflation rate is around 6% p.a. In this case, you need to adjust your target amount for inflation over the entire 20-year period in order to understand how much money you would actually require in the future.

The formula used to calculate the inflation-adjusted goal amount is:

FV = PV (1 + r)^n

Where:

FV = Future Value (Inflation-adjusted goal amount)

PV = Present Value (Current goal amount)

r = Inflation rate

n = Number of years

Applying the values:

FV =1,00,00,000(1+0.06)^20

FV = Rs. 3,20,71,355

This means that Rs.1 Crore today would require approximately Rs.3.21 Crore after 20 years to maintain the same purchasing power.

4. Choosing the Right Funds

The calculations were only the first part of the process. But these numbers become useful only when you choose the right mutual funds for your investments.

Mutual funds are divided into different categories, and each type serves a different purpose. Their risk levels, returns, and overall functionality can vary depending on the kind of fund you select.

In a long-term wealth creation journey, funds that primarily invest in equity are generally the most suitable, as they offer higher growth potential over time. However, even after selecting a fund in the beginning, your portfolio may still require occasional adjustments depending on your goals, market conditions, and investment timeline.

If you are unsure about which fund to select, you can download the Rupeezy app (click on the link) and book a free consultation. Our team will help you choose the right funds based on your investment goals, risk appetite, and timeline.

Now let’s say you have selected the right equity-oriented fund. The next question is: what kind of returns can you expect?

While returns are never guaranteed and can vary based on market conditions and fund selection, historical trends and AMFIs Best Practices Guidelines suggest that equity mutual funds can generate around 12% annual returns over the long term.

However, for our calculations, we will conservatively assume a return of 10% p.a. to account for market fluctuations and the possibility of selecting underperforming funds. This helps create a more realistic wealth creation plan.

5. Determining the Investment Amount

Now that we have arrived at the inflation-adjusted goal amount, the next step is to determine how much you need to invest in order to achieve it. This can be done either through a lump sum investment or through an SIP (Systematic Investment Plan).

The process essentially involves reverse engineering your goal based on your investment duration and expected rate of return.

You can do this easily using the Rupeezy Calculator, where you can enter your goal amount, investment duration, and expected returns to calculate the investment amount required to achieve your target.

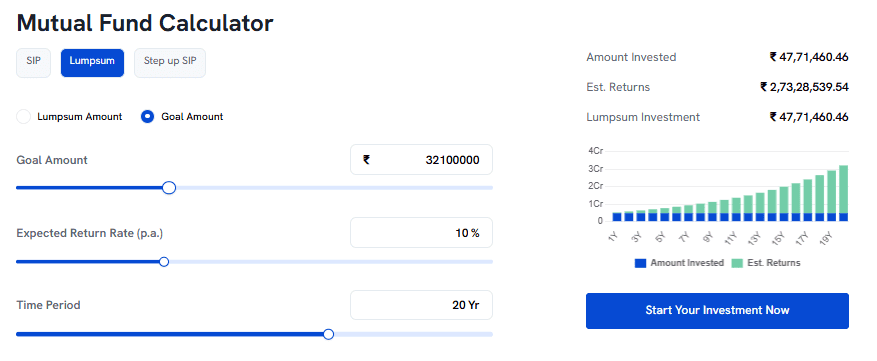

Route A: The Lumpsum Strategy

If you choose the lumpsum route, you would need to invest approximately ?47.7 Lakhs as a one-time investment to build an inflation-adjusted corpus of ?3.21 Crore in 20 years, assuming a return of 10% p.a.

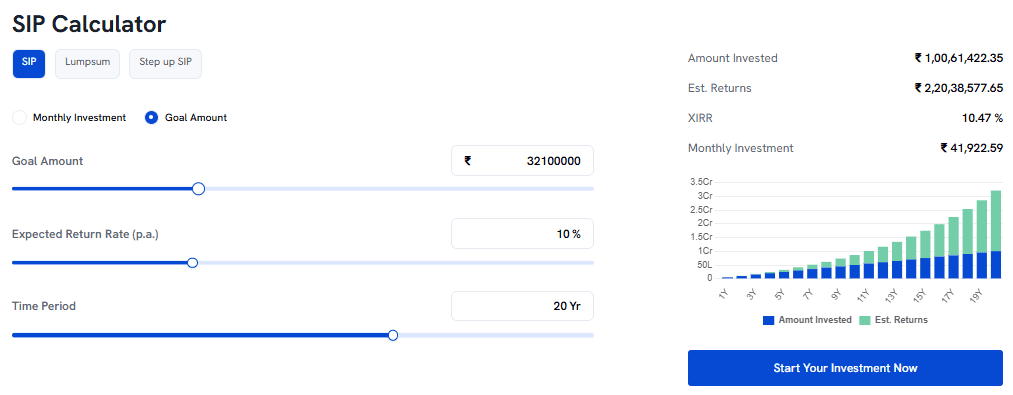

Route B: The SIP route

If you choose the SIP route, you would need to invest approximately ?41,922 every month for 20 years to achieve the same ?3.21 Crore goal, assuming a return of 10% p.a.

Why the Answer Isn’t a Simple Yes or No?

While the math works, these figures are simply not realistic for most salaried individuals, particularly if you are early in your career and managing rent, EMIs, daily expenses, insurance, and other financial commitments alongside your take-home pay.

So, investing nearly Rs.48 Lakhs upfront or committing over Rs.42,000 every month from day one may not feel practical or sustainable. In many cases, this turns into a pressure trap that leaves you overwhelmed and eventually causes you to give up on investing altogether

What Is the Right Approach to Wealth Creation? .

The right approach is not about starting big. It is about starting smart.

One of the biggest mindset mistakes people make is thinking: "If I cannot invest enough to reach my entire goal, there is no point investing at all." That thinking will keep you on the sidelines indefinitely.

The better approach is to start with whatever you can comfortably invest within your current income, and gradually increase that amount every year as your earnings grow. And even if mutual funds do not get you all the way to your goal, they can certainly get you a significant part of the way there, which is far better than not starting at all.

Starting early gives compounding more time to work in your favour, which is why even small SIP amounts can grow into a sizeable corpus over the long term. And if you are starting late, that does not mean you have missed your opportunity. It simply means your plan needs to be more intentional. Higher SIPs and larger step-ups can help bridge the gap, and as your income grows, putting bonuses or surplus savings to work as one-time lumpsum investments can give your corpus an additional push.

At the same time, it is important not to channel every rupee into mutual fund investments. Unlike a savings account, your money here is tied to market cycles, and returns are neither immediate nor guaranteed. If an unexpected expense comes up, you should not be forced to withdraw your long-term investments to manage short-term needs.

This is why wealth creation should be approached with balance. Maintain an emergency fund covering three to six months of expenses, have adequate health and life insurance in place, and then invest the remaining amount across a diversified portfolio. This allows your wealth creation journey to continue without affecting your financial stability.

Conclusion: Can mutual funds make you rich?

Mutual funds alone may not make you rich. But it is the single most powerful catalyst in your wealth creation journey. The real work lies in everything around it: defining your goal, accounting for inflation, choosing the right funds, and investing in a way that is sustainable for you. Get those pieces right, and the math will take care of the rest.

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

Disclaimer

Investments in the securities market are subject to market risks. Read all the related documents carefully before investing. Rupeezy (SEBI RA Registration: INH000013332) provides this content for informational purposes; any securities quoted are for educational display and not as a recommendation. All charts and graphs are based on independent research and reliable sources for the period mentioned within the specific data set. Sometimes we take graphs from external sources. This communication does not promise or assure any fixed, guaranteed, or indicative returns to any client. For our complete registered office address, Member ID, and full SEBI registration details, please refer to our official website.

All Category