What is Behavioral Finance? Concepts, Biases, and Examples

What is Behavioral Finance? Concepts, Biases, and Examples

by Santhosh S

Santhosh is a Finance News Content Writer at Rupeezy with over two years of experience in the finance industry. He holds an MBA in Finance from Jain University. Driven by a deep interest in business, he emphasizes company fundamentals and has strong expertise in stocks, mutual funds, and ETFs.

Last Updated: 24 March, 202610 min read

00:00 / 00:00

At 9:15 a.m. on a Monday morning, Raj stared at his phone as the share market opened. The numbers turned red almost instantly. His heart rate climbed. He had promised himself he would be a long-term investor, someone who believed in patience, discipline, and compounding. Yet his thumb hovered over the “Sell” button.

Just a week earlier, Raj felt confident. News articles were optimistic, his portfolio was up, and investing felt almost easy. Today, fear had taken over. Logic told him markets move in cycles, but emotion murmured something else: get out before it gets worse.

Raj is not careless, uneducated, or reckless.

He is human.

And that is exactly where behavioral finance begins.

Behavioral finance studies how psychology, emotions, and cognitive biases influence financial decisions, often causing investors to act against logic and long-term interests.

For decades, traditional finance assumed investors were perfectly rational, unemotional decision-makers who always acted in their best interest. The reality tells a very different story. Investors panic, follow crowds, hold onto losing stocks, and abandon carefully planned strategies at the worst possible moment. Behavioral finance exists to explain why.

This article explores what behavioral finance is, its core concepts, the most common behavioral finance biases, and real-world examples, all through storytelling that reflects how people actually think and behave with money.

Summary of Behavior Finance What Is Behavioral Finance?

Behavioral finance is the study of how psychological factors, emotions, and cognitive biases influence financial decision-making, helping explain why markets often behave differently from textbook models.

This field gained prominence through the work of psychologists Daniel Kahneman and Amos Tversky, whose research on decision-making under uncertainty revealed that humans rely heavily on mental shortcuts. These shortcuts, while helpful in daily life, often lead to predictable errors when applied to investing.

Their work later formed the foundation of behavioral finance theory, which combines psychology and economics to explain market anomalies, bubbles, crashes, and everyday investing mistakes.

Behavioral finance rests on several key ideas that explain how investors actually behave.

Investors Are Human, Not Perfectly Rational: Traditional finance assumes investors are rational and unemotional, but behavioral finance shows that emotions, personal experiences, beliefs, and social cues influence real investors. Rather than making purely logical decisions, most investors behave in ways that reflect fear, confidence, regret, and social pressure.

Cognitive Errors Are Systematic: Behavioral finance demonstrates that investing mistakes are not random. They follow identifiable psychological patterns shaped by how the human brain processes information under uncertainty. Because these errors repeat consistently across investors, they can be studied, anticipated, and managed.

Emotions Drive Risk Perception: Risk is not perceived objectively. The same investment can feel safe during a rising market and dangerous during a downturn, even when its fundamentals remain unchanged. Emotional states often determine how much risk an investor believes they are taking.

Heuristics and Mental Shortcuts: Behavioral finance explains that investors rely on simplified mental rules to make decisions in uncertain situations. While these shortcuts help process complex information quickly, they often lead investors to ignore deeper analysis, rely on recent or familiar information, and make judgments that deviate from objective financial logic.

Common Behavioral Finance Biases

Understanding behavioral finance biases is essential for improving decision-making. Many of these biases are interconnected and often reinforce one another.

These behavioral finance biases are not isolated mistakes; they are recurring psychological patterns that influence investors across markets, asset classes, and generations.

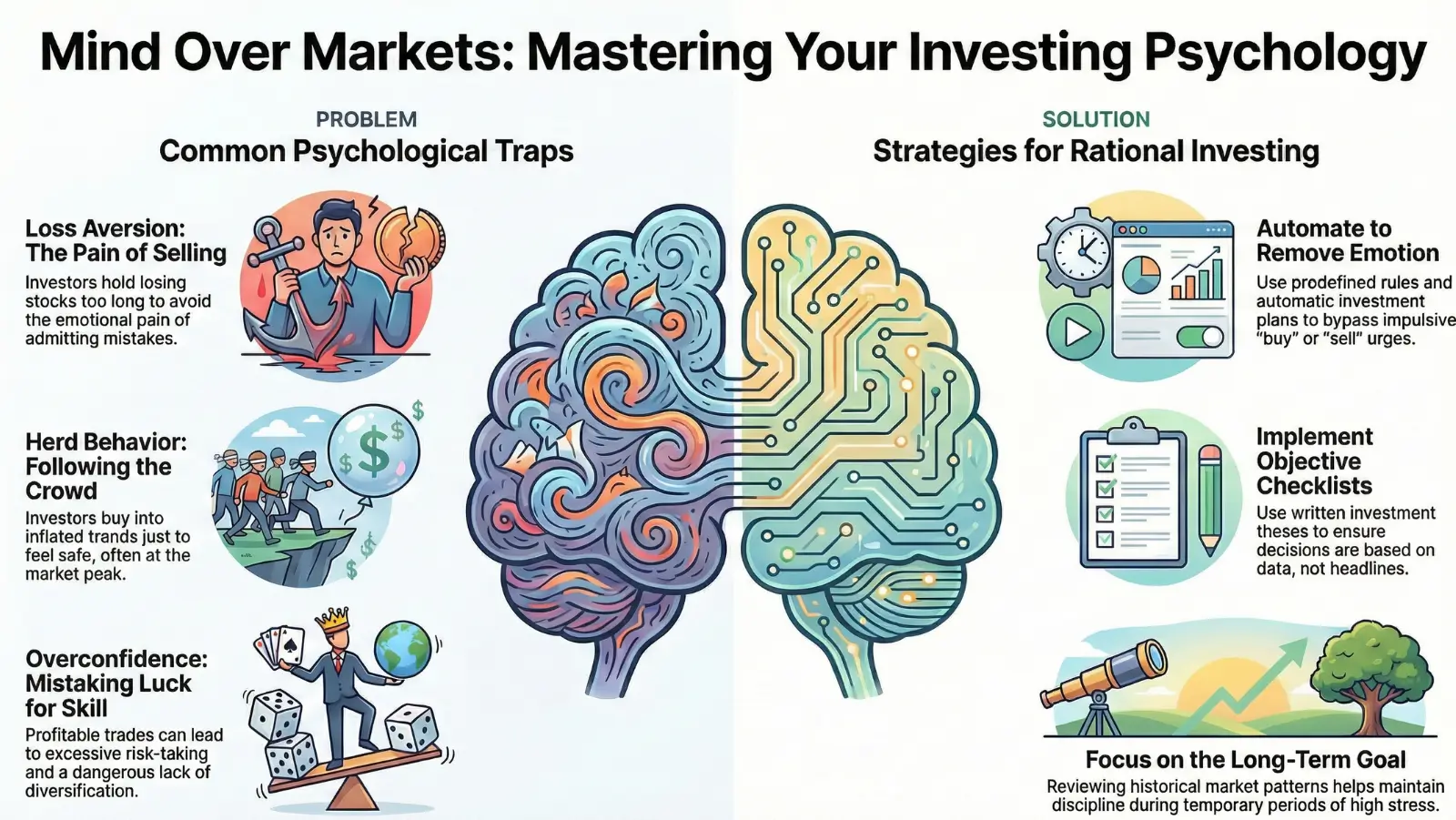

1) Loss Aversion: Loss aversion explains why investors often hold on to losing stocks far longer than they should, even when long-term investment logic suggests otherwise.

Imagine buying a stock at Rs 1,000 and watching it fall to Rs 700. Selling now feels painful, not because the business is sound, but because selling would mean admitting a mistake. Many investors wait, hoping only to break even, even as fundamentals worsen.

During market crashes, this same bias pushes investors to sell everything at the worst possible moment, simply to escape emotional pain.

2) Overconfidence Bias: Overconfidence bias occurs when investors begin to believe that their success is driven entirely by skill rather than favorable market conditions.

After a few profitable decisions, confidence grows, caution fades, and risk-taking increases. Investors may trade more frequently, concentrate their portfolios, or ignore diversification, convinced they can predict outcomes. When markets change, this misplaced confidence often leads to larger losses than anticipated.

3) Herd Behavior: Herd behavior emerges when investors look to others for reassurance during uncertainty.

Rising prices create a sense of safety, not because value has improved, but because “everyone else is buying." Investors join the trend to avoid missing out, often without understanding the underlying business. By the time widespread participation feels comfortable, prices are often already inflated, setting the stage for sharp reversals.

4) Confirmation Bias: Confirmation bias makes investors selectively absorb information that supports their existing beliefs.

Once an opinion is formed about a stock, positive news is embraced while negative signals are ignored. Weak earnings, rising debt, or industry disruption are dismissed as temporary issues. This bias prevents investors from reassessing decisions objectively, even when evidence clearly changes.

5) Anchoring Bias: Anchoring bias occurs when investors fixate on an initial reference point, such as a purchase price or a stock’s previous high.

A stock that once traded at Rs 1,500 but now trades at Rs 900 may feel cheap, even if the company’s fundamentals have deteriorated. By anchoring decisions to outdated numbers, investors fail to evaluate current value objectively.

6) Familiarity Bias: Familiarity bias reflects the natural preference for what feels known and comfortable.

Investors often concentrate their portfolios in domestic stocks, well-known brands, or even their employer’s shares, believing familiarity reduces risk. In reality, this comfort comes at the cost of diversification, increasing exposure to concentrated and avoidable risks.

7) Recency Bias: Recency bias happens when investors place excessive importance on recent events while ignoring long-term historical patterns and underlying fundamentals.

After a strong market rally, investors may assume high returns will continue indefinitely and increase risk exposure, believing recent performance reflects future outcomes. When markets reverse, this overreliance on recent trends often leads to poor timing decisions and avoidable losses.

8) Endowment Effect: Endowment effect occurs when investors assign greater value to investments simply because they own them, rather than based on objective analysis.

An investor may continue holding a stock despite weakening fundamentals because ownership creates emotional attachment. This attachment makes selling feel like a loss, causing investors to overvalue familiar holdings and retain underperforming assets longer than rational analysis would suggest.

Behavioral Finance and Market Cycles

Market cycle booms and busts are driven as much by psychology as by economics. This pattern was clearly visible during the 2008 global financial crisis, when panic-driven selling pushed markets far below their intrinsic value.

During bull markets, overconfidence and herd behavior dominate. During bear markets, loss aversion and panic selling take over. Behavioral finance explains why investors consistently buy high and sell low, despite knowing better.

Value Investing and Behavioral Finance

The relationship between value investing and behavioral finance is deeply intertwined. Value investing thrives on market inefficiencies created by emotional overreactions.

When fear grips the market, prices may fall below intrinsic value. When optimism becomes excessive, prices may exceed fundamentals. Value investors aim to remain rational, while others act emotionally.

Investors such as Benjamin Graham highlighted the importance of temperament over intelligence. Warren Buffett has repeatedly noted that successful investing requires emotional stability.

In this sense, value investing is an applied form of behavioral finance, one that seeks to exploit psychological mispricing while avoiding common biases.

This connection between value investing and behavioral finance highlights how disciplined investors can benefit by remaining rational when markets are driven by emotion.

COVID-19 Market Crash

The COVID-19 pandemic highlighted behavioral finance in real time. Markets experienced extreme volatility, driven by uncertainty and fear. Many investors sold at the worst possible moment, while others chased speculative assets fuelled by online narratives.

Social media intensified behavioral biases, accelerating herd behavior and overconfidence. These patterns were not anomalies; they were predictable outcomes of human psychology under stress.

Why Behavioral Finance Matters More Than Ever

Today’s investors operate in an environment very different from that of previous generations. Markets are no longer something you check once a day in the newspaper. Prices update every second, news breaks instantly, and opinions flood social media.

This constant stimulation increases emotional reactions. Fear spreads faster. Euphoria lasts longer. Small pieces of information are often treated as decisive signals. Behavioral finance helps explain why access to more information does not automatically lead to better decisions.

From a practical standpoint, behavioral finance matters because most long-term investment outcomes are determined not through intelligence, education, or access to data, but by their own behavior during periods of stress and uncertainty. The biggest mistakes tend to occur during extremes: market peaks and market crashes.

Various financial advisors, policymakers, and institutions increasingly rely on behavioral insights to design better systems. Examples like automatic investment plans, default asset allocations, and simplified choices that reduce decision paralysis. These approaches acknowledge a core truth that systems should be built for normal human behavior and not to idealize rationality.

Investors can apply behavioral finance principles in practice by following a few disciplined steps:

Creating predefined rules for buying and selling to reduce emotional reactions.

Using written investment theses and checklists to counter confirmation bias.

Automating investments to avoid timing decisions.

Focusing on long-term goals rather than short-term price movements.

Reviewing past decisions to identify recurring behavioral patterns.

For example, an investor who commits to rebalancing a portfolio once a year avoids emotional decisions during periods of market volatility.

These kinds of simple systems do not remove human bias, but they help investors make better decisions by limiting emotional reactions during uncertain periods.

Can Behavioral Biases Be Eliminated?

A common misconception is that understanding behavioral finance will eliminate biases. In reality, biases are deeply rooted in human psychology and evolved as survival mechanisms. They helped humans make quick decisions in uncertain environments long before financial markets existed.

The goal of behavioral finance is not perfection, but improvement. Investors who accept their limitations can design processes that protect them from their worst instincts.

This might include limiting portfolio checks, avoiding constant financial news, or setting strict rebalancing schedules. Over time, small behavioral improvements compound just like financial returns.

Conclusion

When Raj finally lowered his phone, he chose not to act on impulse. Instead, he revisited his long-term plan, reminding himself why he invested in the first place. The market would continue to fluctuate, but his behavior would ultimately determine the outcome.

This is the central insight of behavioral finance.

Markets are shaped by numbers but driven by people. And understanding the psychology behind financial decisions, through behavioral finance theory, awareness of behavioral finance biases, and the discipline practiced in value investing and behavioral finance, may be the most powerful investment advantage of all.

For individual investors, combining behavioral awareness with tools that promote discipline can make a meaningful difference. Brokerage platforms such as Rupeezy, highlight structured investing that can play a role in helping investors to stay focused on long-term objectives.

Note: This article is written for educational purposes and reflects widely accepted research in behavioral finance, including the work of Daniel Kahneman, Amos Tversky, and leading value investors. It is not intended as financial advice. Readers should consider their own financial circumstances or consult a qualified professional before making investment decisions.

FAQs:

Q1) What is behavioral finance?

Behavioral finance studies how psychology, emotions, and cognitive biases influence financial decisions, often causing investors to act against logic and long-term interests.

Q2) Why do investors panic or make poor decisions during market crashes?

Investors panic because of fear, loss aversion, and herd behavior distort risk perception and push people to sell at the worst possible moments.

Q3) What are the most common behavioral finance biases?

Common biases include loss aversion, overconfidence, herd behavior, confirmation bias, anchoring, familiarity bias, recency bias, and the endowment effect.

Q4) How is behavioral finance connected to value investing?

Value investing uses behavioral finance insights by staying rational during emotional market swings and taking advantage of mispricing caused by fear and overconfidence.

Q5) Can behavioral biases be completely eliminated?

No, behavioral biases cannot be eliminated, but they can be managed through awareness, discipline, and structured investing processes.

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

Want to start investment?

Open Rupeezy account now. It is free and 100% secure.