Is Amanta Healthcare IPO Good or Bad – Detailed Review

00:00 / 00:00

Amanta Healthcare Limited's IPO is set to open its initial public offering from September 01, 2025, to September 03, 2025. When considering applying for this IPO, potential investors might have questions about whether the Amanta Healthcare IPO is a good investment and if it's worth subscribing to.

This article provides a comprehensive Amanta Healthcare IPO review, covering its business operations and fundamental analysis to help you make an informed investment decision.

Amanta Healthcare IPO Review

Amanta Healthcare Limited's IPO is a book-built issue of Rs 126 crore, consisting entirely of a fresh issue of 1 crore shares. The IPO will be open for subscription from September 1 to September 3, 2025, with a price band of Rs 120 to Rs 126 per share and a lot size of 119 shares. The company plans to use the net proceeds to fund capital expenditures for new manufacturing lines for SteriPort and Small Volume Parenterals (SVP) at its facility in Hariyala, Gujarat, and for general corporate purposes.

Amanta Healthcare is a pharmaceutical company that specializes in manufacturing sterile formulations, including IV fluids and injectables, using advanced technologies like Aseptic Blow-Fill-Seal (ABFS) and Injection Stretch Blow Moulding (ISBM). The company's product portfolio covers six therapeutic segments and is distributed both domestically through a network of over 320 distributors and internationally to 21 countries.

Financially, Amanta Healthcare has shown a significant turnaround. The company went from a net loss of Rs 2.11 crore in FY23 to a profit of Rs 10.50 crore in FY25. This profitability was driven by a strong EBITDA margin of 22.11% in FY25, which reflects improved operational efficiency and cost control. While revenue saw a slight dip in FY25, the company has successfully improved its financial metrics, including its Return on Equity (RoE) and Return on Capital Employed (RoCE). Compared to its peer, Denis Chem Lab, Amanta has a larger scale of operations and better operational efficiency, as indicated by its EBITDA and return metrics, but it also carries a higher debt-to-equity ratio.

Key strengths of the company include its established presence in the sterile formulations segment, a diversified product portfolio, and experienced management. However, potential investors should be aware of risks such as the reliance on a single manufacturing facility, high finance costs, dependence on key suppliers, and regulatory and litigation risks. The IPO provides the company with an opportunity to expand its manufacturing capabilities and support future growth.

Company Overview of Amanta Healthcare IPO

Amanta Healthcare is an Indian pharmaceutical company specializing in sterile formulations, with a focus on intravenous (IV) fluids and injectables. The company manufactures Large Volume Parenterals (LVP), Small Volume Parenterals (SVP), and SteriPort products using aseptic processing technology at its WHO-GMP compliant facility located in Hariyala, Gujarat. Its product portfolio covers critical care, nephrology, gastroenterology, and other therapeutic areas. The company distributes its products across India through a network of more than 320 distributors and also exports to 21 international markets.

As of March 31, 2025, Amanta Healthcare markets more than 45 products, catering to both domestic and overseas healthcare providers. The company has a strong presence in institutional sales to government hospitals, private healthcare institutions, and also supplies to international aid organizations. Its ability to comply with stringent global regulatory requirements positions it competitively in the sterile formulations segment.

The company’s leadership includes experienced promoters and professionals with deep expertise in the pharmaceutical industry. Amanta Healthcare has successfully transitioned from a loss-making position in FY23 to consistent profitability by FY25, driven by margin improvement, operational efficiency, and capacity utilization.

Industry Overview of Amanta Healthcare IPO

Amanta Healthcare operates within the broader Indian pharmaceutical industry, with a particular focus on the sterile IV fluids and injectables segment. The industry was valued at around USD 45 to 47 billion in FY24 and is projected to grow at a CAGR of 9 to 11% between fiscals 2024 and 2029, supported by rising healthcare expenditure, increasing prevalence of chronic diseases, and government initiatives such as the Production Linked Incentive (PLI) scheme.

The IV fluids segment is experiencing consistent growth, driven by rising demand in hospitals for critical care, surgical procedures, trauma management, and emergency medicine. The global IV fluids market is also expanding, and creating opportunities for Indian manufacturers due to their cost competitiveness and compliance with international quality standards.

Exports from India are also witnessing strong momentum, as the country maintains its position as a leading supplier of affordable and quality generics. Demand from semi-regulated and regulated markets is expected to increase, further supporting the sterile formulations segment where Amanta Healthcare operates.

Financial Overview of Amanta Healthcare IPO

Particulars | March 31, 2025 (Rs crore) | March 31, 2024 (Rs crore) | March 31, 2023 (Rs crore) |

Revenue from Operations | 274.71 | 280.34 | 259.13 |

EBITDA | 61.05 | 58.76 | 56.31 |

EBITDA Margin (%) | 22.11% | 20.86% | 21.43% |

PAT | 10.5 | 3.63 | -2.11 |

PAT Margin (%) | 3.86% | 1.30% | -0.82% |

RoE (%) | 12.42% | 5.27% | -3.27% |

RoCE (%) | 13.72% | 12.76% | 12.19% |

The financial performance of Amanta Healthcare over the three fiscal years ending March 31, 2023, 2024, and 2025, highlights a clear turnaround in profitability and improved operating efficiency.

Revenue from operations grew from Rs 259.12 crore in FY23 to Rs 280.34 crore in FY24, reflecting healthy demand. However, FY25 saw a slight dip to Rs 274.70 crore, which the company attributes to market pressures. Despite this, the company has successfully maintained stable top-line performance across the period.

EBITDA has shown strong growth, improving from Rs 56.30 crore in FY23 to Rs 61.05 crore in FY25. The EBITDA margin expanded from 21.43% in FY23 to 22.11% in FY25, underscoring better cost optimization, operational leverage, and an improved product mix. This consistent margin expansion is a positive indicator of operational strength.

Profit After Tax (PAT) reflects a major turnaround. The company moved from a net loss of Rs 2.11 crore in FY23 to a profit of Rs 3.63 crore in FY24 and further to Rs 10.50 crore in FY25. This demonstrates Amanta’s ability to translate margin improvements into bottom-line growth. However, the PAT margin of 3.86% in FY25, though an improvement, remains modest. The significant loss in FY23 was primarily due to a one-time write-off of deferred tax assets.

Return metrics show improvement but highlight the scope for stronger shareholder returns. Return on Capital Employed (RoCE) improved from 12.19% in FY23 to 13.72% in FY25, pointing to more efficient use of capital. Return on Net Worth (RoNW) also turned positive and improved to 10.89% in FY25, though it remains relatively low due to the company’s modest profit base.

In summary, Amanta Healthcare has achieved a financial turnaround marked by higher margins and profitability, despite marginal revenue contraction in FY25. The company’s strength lies in operational efficiency and cost control, but scaling up revenues and improving net margins will be key to matching larger peers in the sector.

Strengths and Risks of Amanta Healthcare IPO

Let's delve into the strengths and weaknesses to assess if the Amanta Healthcare IPO is good or bad for investors.

Strengths

Established Presence in Sterile Formulations: Amanta Healthcare is a recognized manufacturer of sterile liquid products, including IV fluids and injectables. The company's manufacturing facility is ISO and WHO-GMP certified, demonstrating a commitment to quality and compliance with international standards.

Diverse Product Portfolio and Markets: The company has a well-diversified portfolio of over 47 products across six therapeutic segments. It serves both the domestic market through a network of over 320 distributors and exports to more than 21 countries, including in Africa, Latin America, and the UK, diversifying its revenue streams.

Turnaround in Profitability and Margin Expansion: Amanta Healthcare has successfully transitioned from a net loss of Rs 2.11 crore in Fiscal 2023 to a profit of Rs 10.50 crore in Fiscal 2025. This is supported by a growing EBITDA, which increased from Rs 56.30 crore in FY23 to Rs 61.05 crore in FY25, reflecting improved operational efficiency.

Strong Manufacturing Capabilities: The company's large manufacturing facility in Hariyala, Gujarat, utilizes advanced technologies such as Aseptic Blow-Fill-Seal (ABFS) and Injection Stretch Blow Moulding (ISBM), allowing for flexible production across a wide range of volumes (2ml to 1000ml) and product types.

Experienced Management: The company is led by an experienced management team, including its promoter and Managing Director, Bhavesh Patel, who has over 30 years of industry experience. This leadership provides a strategic advantage and domain expertise in the competitive pharmaceutical market.

Risks

Single Manufacturing Facility: All manufacturing operations are concentrated at a single facility in Hariyala, Gujarat. This creates a significant risk of business disruption from a single event, such as a natural disaster, machinery breakdown, or regulatory issue.

High Finance Costs: The company has a high level of debt, with finance costs making up a significant portion of its earnings. In Fiscal 2025, finance costs constituted 45.78% of the company's EBITDA, which could strain cash flows and limit the ability to fund new projects.

Dependence on Key Suppliers and Raw Materials: The company relies on a limited number of suppliers for key raw materials, such as LDPE and PP granules, which are subject to volatile crude oil prices. Disruptions in the supply chain or price fluctuations could adversely affect business operations and financial condition.

Regulatory and Litigation Risks: As a pharmaceutical company, Amanta Healthcare is subject to extensive regulations. The company has faced past issues, including a two-day suspension of its manufacturing license and ongoing material litigation, which could divert management's attention and impact its reputation.

High Employee Attrition: The company has experienced high attrition rates for its full-time employees, with a rate of 9.88% in Fiscal 2025, 25.90% in Fiscal 2024, and 33.82% in Fiscal 2023. This could pose challenges in attracting and retaining a skilled workforce, potentially impacting operations.

Strategies of Amanta Healthcare IPO

Capacity Expansion: The company plans to utilize the IPO proceeds to fund capital expenditure for new SteriPort and SVP manufacturing lines at its Hariyala facility. This expansion is intended to increase production volumes and meet growing demand.

Enhance Product Portfolio: Amanta Healthcare aims to develop new formulations and improve existing ones through its dedicated R&D and quality control laboratories. The goal is to broaden its product portfolio and introduce more complex and specialized sterile liquid solutions.

Strengthen Domestic and International Sales Network: The company's strategy is to expand its domestic sales and distribution network and grow its international sales by targeting new markets and increasing its presence in existing ones, such as Africa, Latin America, and the UK.

Improve Operational Efficiency: By investing in new machinery and adopting modern technologies, the company seeks to enhance its manufacturing processes. This includes a focus on automation and streamlining workflows to improve efficiency and maintain strong profit margins.

Leverage Industry Growth: With increasing demand for IV fluids and sterile injectables due to rising healthcare expenditure and the prevalence of chronic diseases in both domestic and global markets, Amanta Healthcare is strategically positioned to capitalize on these favorable industry trends.

Amanta Healthcare IPO vs. Peers

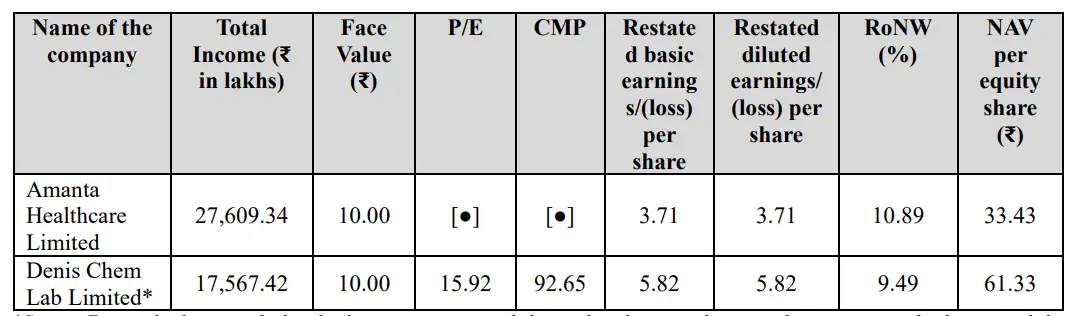

Source: RHP of the company

In Fiscal 2025, Amanta Healthcare reported total income of Rs 276.09 crore, while its listed peer, Denis Chem Lab Limited, reported a total income of Rs 175.67 crore. Amanta Healthcare's revenue from operations saw a slight decrease from Rs 280.34 crore in FY24 to Rs 274.70 crore in FY25, whereas Denis Chem Lab's revenue grew at a CAGR of 3.82% during the same period.

Amanta Healthcare's profitability metrics are strong, demonstrating its operational efficiency. For Fiscal 2025, its EBITDA margin was 22.11%, significantly higher than Denis Chem Lab's 10.52%. However, its PAT margin of 3.86% was lower than Denis Chem Lab's 4.66% in FY25.

The company's return metrics show a positive trend. Amanta Healthcare's RoCE increased from 12.19% in FY23 to 13.72% in FY25, while Denis Chem Lab's stood at 13.53% in FY25. Amanta's RoNW also saw significant improvement, rising to 10.89% in FY25, which is higher than Denis Chem Lab's 9.49% for the same period. This indicates Amanta Healthcare's efficient use of capital and better returns on net worth.

Amanta Healthcare's debt-to-equity ratio of 2.02 for Fiscal 2025, while improved from 3.43 in FY23, is significantly higher than Denis Chem Lab's low ratio of 0.01. This suggests that Amanta Healthcare relies more on debt to finance its operations. The company's management has confirmed that its liquidity is adequate.

Overall, while Amanta Healthcare has a larger scale of operations and better operational efficiency as reflected in its EBITDA and return metrics, its higher reliance on debt and lower net profit margin compared to its peer are key areas for consideration.

Objectives of Amanta Healthcare IPO

The offer comprises only a fresh issue. The net proceeds from the fresh issue of Rs 721 crore are proposed to be utilised for:

Funding Capital Expenditure for manufacturing plant construction, plant and equipment purchases for SteriPort at Hariyala, Kheda, Gujarat, amounting to Rs 70 crores.

Funding Capital Expenditure for manufacturing plant construction, plant and equipment purchases for Small Volume Parenterals (SVP) at Hariyala, Kheda, Gujarat, amounting to Rs 30.13 crores.

General corporate purposes.

Amanta Healthcare IPO Details

IPO Dates

Amanta Healthcare IPO will be open for subscription from September 01, 2025, to September 03, 2025. The allotment of shares to investors will take place on September 04, 2025, and the company is expected to be listed on the NSE and BSE on September 09, 2025.

IPO Issue Price

Amanta Healthcare is offering its shares in the price band of Rs 120 to Rs 126 per share. This means you would require an investment of Rs. 14,994 per lot (119 shares) if you are bidding for the IPO at the upper price band.

IPO Size

Amanta Healthcare is planning to raise through only fresh issue of 1,00,00,000 shares, which are worth Rs 126 crores.

IPO Allotment Status

Investors who applied for the IPO can check their IPO allotment status on September 04, 2025, through the registrar's website, MUFG Intime India Private Limited, BSE, NSE, or through the stockbroker platform.

IPO Listing Date

The shares of Amanta Healthcare will be listed on the NSE and BSE on September 09, 2025.

IPO Application Link

Open demat account with Rupeezy today and enjoy a seamless experience when applying for the IPO. With an easy-to-use platform, Rupeezy makes the IPO application process quick and hassle-free.

Apply for Amanta Healthcare IPO

Important IPO Details | |

Bidding Date | September 01, 2025 to September 03, 2025 |

Allotment Date | September 04, 2025 |

Listing Date | September 09, 2025 |

Issue Price | Rs 120 to Rs 126 per share |

Lot Size | 119 Shares |

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

All Category