Is Indogulf Cropsciences IPO Good or Bad - Detailed Review

00:00 / 00:00

Indogulf Cropsciences Limited IPO is kicking off its initial public offering, which will be open from June 26, 2025, to June 30, 2025. While considering applying for this IPO, certain questions may arise in your mind, including whether the Indogulf Cropsciences IPO is good or bad, whether it is worth investing in this IPO, and so on.

This article offers a comprehensive Indogulf Cropsciences IPO review, covering its business operations and fundamental analysis to help you make an informed investment choice.

Indogulf Cropsciences IPO Review

Indogulf Cropsciences is gearing up for its Initial Public Offering (IPO), aiming to raise Rs 200 crore. The proceeds are primarily earmarked to be utilised towards meeting working capital requirements, partial or full repayment of existing borrowings, capital expenditure for establishing an in-house dry flowable (DF) plant at Barwasni, Sonipat, Haryana, and for general corporate purposes.

When we look at the financials of the company, Indogulf Cropsciences showed stable growth with revenue increasing from Rs. 487.21 crore in FY22 to Rs. 552.23 crore in FY24. EBITDA and PAT also improved, with margins recovering after a dip in FY23. Additionally, the return ratios like RoNW and RoCE strengthened in FY24. For the nine months ended December 2024, the company reported Rs. 464.19 crore in revenue and Rs. 21.68 crore in PAT.

Observing the peer comparisons, Indogulf Cropsciences reported revenue of Rs. 552.23 crore, placing it ahead of some peers like Basant Agro and Aries Agro, while trailing larger players like Best Agrolife and Heranba. Its EPS of Rs. 12.00 aligns with mid-performing peers and outpaces several others. The company’s RoNW of 12.19% reflects comparatively better capital efficiency, outperforming many peers but remaining below top players like Best Agrolife and India Pesticides.

That said, potential investors are strongly advised to conduct their own independent analysis and consult financial advisors before making any investment decision. Keep reading to find out more about the company’s background, business model, and growth strategy.

Company Overview of Indogulf Cropsciences IPO

Indogulf Cropsciences is a company that is engaged in the manufacturing of crop protection products, plant nutrients, and biologicals in India. It is recognized as one of the early indigenous producers of Pyrazosulfuron Ethyl technical with a minimum purity of 97%, with commercial production starting in 2018. Since its inception in 1993, the company has grown steadily and now exports its products to over 34 countries, establishing itself as a growing player in the global agrochemical market.

Operating under three main business verticals, crop protection, plant nutrients, and biologicals, the company serves both retail and institutional customers, focusing on enhancing crop yield and promoting sustainable farming practices. Its product portfolio spans a wide range of formulations such as Water Dispersible Granules (WDG), Suspension Concentrate (SC), Capsule Suspension (CS), Ultra Low Volume (ULV), Emulsion in Water (EW), Soluble Granule (SG), and Flowable Suspension (FS), offered in powder, granule, and liquid forms.

The company’s offerings cater to various crop types, including cereals, pulses, oilseeds, fibre crops, fungicides, herbicides, plant growth regulators, and efficacy enhancers, available in both formulation and technical forms. Key products in this category include Lambda Cyhalothrin 5% EC (Farrate), Tembotrione 34.4% SC (Alkazar), and Glyphosate 41% SL (Bound Off).

In the biologicals segment, the company produces innovative bio-stimulants designed to support pest and disease management, improve stress resistance, and enhance nutrient efficiency. Key biological products include seaweed extract (Breeza), humate (Apache), mycorrhiza (Root-o-Max Gold), and combination products (Empire). The plant nutrients vertical focuses on improving soil fertility and boosting crop health through the manufacture of straight fertilizers and nutrient deficiency correctors. Notable products include Picaso Gold, Picaso Power, and Jagromin-99.

With four manufacturing facilities across Jammu & Kashmir and Haryana, and two subsidiaries—one in Australia and another in India—the company also offers customized contract manufacturing.

Industry Overview of Indogulf Cropsciences IPO

Globally, the pesticide industry is led by the herbicide segment, followed by fungicides and insecticides. Out of the total global crop protection market valued at approximately USD 6904 crore, herbicides alone contribute nearly 50%. However, in India, herbicide usage is comparatively lower, accounting for just around 17% of the country's total pesticide consumption.

Beyond the agricultural sector, the non-crop segment also plays a significant role in the global pesticides market. In 2023, this segment was valued at approximately USD 1100 crore. Non-crop pesticides are commonly used in areas such as home and garden care, turf and ornamental maintenance, pest control services, industrial vegetation management, forestry, public health, and aquatic environments. These products help manage weeds, pests, and diseases and are also used as plant growth regulators.

Driven by their diverse applications and the benefits they offer, non-crop pesticide demand is expected to grow steadily. However, the crop protection segment is projected to expand at a comparatively faster pace. The global non-crop pesticides market is anticipated to grow at a CAGR of about 4.1% to 5% and reach approximately USD 1400 crore by 2028.

Financial Overview of Indogulf Cropsciences IPO

Particulars | December 31, 2024 | March 31, 2024 | March 31, 2023 | March 31, 2022 |

Revenue from operations (Rs Cr) | 464.19 | 552.23 | 549.66 | 487.21 |

EBITDA (Rs. Cr) | 44.78 | 55.74 | 49.04 | 47.24 |

EBITDA Margin (%) | 9.65% | 10.09% | 8.92% | 9.70% |

PAT (Rs. Cr) | 21.68 | 28.23 | 22.42 | 26.36 |

PAT Margin (%) | 4.67% | 5.11% | 4.08% | 5.41% |

RoNW (%) | 8.17% | 12.19% | 11.03% | 14.60% |

RoCE (%) | 8.07% | 11.93% | 10.12% | 13.81% |

Indogulf Cropsciences demonstrated a steady growth in its revenue from operations, rising from Rs. 487.21 crore in FY22 to Rs. 549.66 crore in FY23, and marginally to Rs. 552.23 crore in FY24.

The company’s EBITDA followed a positive trend, increasing from Rs. 47.24 crore in FY22 to Rs. 49.04 crore in FY23 and reaching Rs. 55.74 crore in FY24. Correspondingly, the EBITDA margin improved from 9.70% in FY22 to 10.09% in FY24, despite a dip to 8.92% in FY23.

The Profit After Tax (PAT) moved from Rs. 26.36 crore in FY22 down to Rs. 22.42 crore in FY23 and then rose to Rs. 28.23 crore in FY24. The dip in FY23 aligns with an increase in expenses (as seen in the P&L). This is also reflected in the PAT margin trend, which dipped to 4.08% in FY23 but recovered to 5.11% in FY24.

When it comes to return ratios, the Return on Net Worth declined from 14.60% in FY22 to 11.03% in FY23 but improved to 12.19% in FY24. Similarly, Return on Capital Employed followed a comparable pattern, falling from 13.81% in FY22 to 10.12% in FY23 before rising to 11.93% in FY24.

Currently, for the nine months ended December 31, 2024, Indogulf Cropsciences reported revenue from operations of Rs. 464.19 crore. The EBITDA for this period stood at Rs. 44.78 crore with a margin of 9.65%. The company recorded PAT of Rs. 21.68 crore, representing a PAT margin of 4.67%.

Strengths and Risks of Indogulf Cropsciences IPO

Let’s dive into the strengths and weaknesses to assess if the Indogulf Cropsciences IPO is good or bad for investors.

Strengths

Diverse product portfolio and innovation:

With over 260 products across crop protection, plant nutrients, and biologicals, the company leverages in-house innovation, patented packaging, and strong branding to serve domestic and global markets effectively.Extensive distribution network:

The company operates a robust distribution network across 22 Indian states, 3 Union Territories, and over 34 countries, supported by 6,916 domestic distributors, 192 institutional partners, and 143 international partners.Backward integrated manufacturing:

With four ISO-certified facilities and in-house production of key active ingredients, the company’s backward integration enhances cost efficiency, reduces supplier dependence, and enables flexible, multi-purpose manufacturing across all product verticals.Robust R&D capabilities:

With a NABL-accredited lab and a skilled team, the company drives innovation through continuous product development, process improvements, and advanced technologies, supporting a strong and diverse product pipeline.

Risks

Supply chain risk:

Dependence on third-party suppliers for raw materials exposes the company to cost volatility and supply disruptions, which may impact production, pricing, and overall financial performance.Working capital uncertainty:

Planned deployment of Rs 65 crore towards working capital is based on assumptions that may not hold, potentially impacting liquidity, operations, and profitability.Seasonal and policy risk:

The agrochemical business is highly dependent on weather conditions and government policies, due to which adverse climate events or changes in agricultural subsidies may significantly impact operations and profitability.Customer concentration risk:

Reliance on a limited number of key customers may lead to revenue volatility, where order cancellations, payment delays, or inability to diversify the customer base could adversely impact profitability and cash flows.Manufacturing disruption risk:

Any unplanned shutdowns, accidents, or regulatory issues at manufacturing facilities could significantly impact production, lead to financial losses, and disrupt operations.

Strategies of Indogulf Cropsciences IPO

Capacity expansion for efficiency:

The company plans to expand its Barwasni facility with a new in-house dry flowable plant, enhancing production capacity, cost efficiency, and product versatility across all three segments.Expanding product portfolio:

The company aims to grow its product range across crop protection, plant nutrients, and biologicals by leveraging R&D, launching new offerings, and entering new markets to boost revenue, profitability, and market share.Enhancing R&D capabilities:

The company continues to invest in R&D to drive innovation, expand its product portfolio, reduce costs, and improve sustainability through a structured short, mid, and long-term development strategy.Strategic collaborations:

Through partnerships with research institutions and government bodies, the company adds 15–20 new products annually, driving innovation, expanding market reach, and strengthening long-term competitiveness in the agriculture sector.Expanding global reach:

The company aims to strengthen its domestic and international distribution network, enhance market penetration through its subsidiary AGPL, and secure foreign product registrations to drive growth and tap into high-volume export markets.Cost optimization strategy:

The company focuses on enhancing operational efficiency through process automation, in-house integration, supply chain improvements, and strategic expansion to reduce costs, improve margins, and boost profitability.

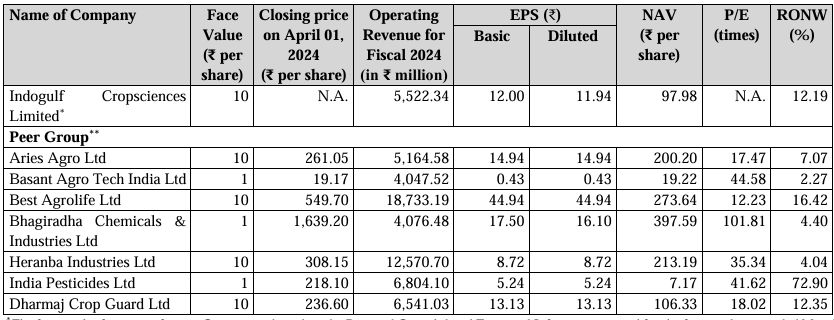

Indogulf Cropsciences IPO Vs Peers

Source: RHP of the company

In terms of scale, Indogulf Cropsciences reported an operating revenue of Rs. 552.23 crore in Fiscal 2024, which is lower than certain peers such as Best Agrolife Ltd (Rs. 1,873.32 crore), and Heranba Industries Ltd (Rs. 1,257.07 crore). But it remains comparable with Basant Agro (Rs. 404.75 crore), Bhagiradha Chemicals (Rs. 407.64 crore), Aries Agro Ltd (Rs. 516.46 crore), Dharmaj Crop Guard (Rs. 654.10 crore), and India Pesticides Ltd (Rs. 680.41 crore).

The company reported an EPS (Basic) of Rs. 12.00 in Fiscal 2024. This is broadly in line with peers such as Dharmaj Crop Guard Ltd (Rs. 13.13), Aries Agro Ltd (Rs. 14.94), though lower than Bhagiradha Chemicals & Industries Ltd (Rs. 17.50) and Best Agrolife Ltd (Rs. 44.94). But it is far better than Basant Agro (Rs. 0.43), Heranba (Rs. 8.72), and India Pesticides (Rs. 5.24).

The Return on Net Worth (RoNW) for Fiscal 2024 stood at 12.19%, reflecting a relatively better capital efficiency. This RoNW is higher than that of Heranba Industries Ltd (4.04%), Bhagiradha Chemicals & Industries Ltd (4.40%), and Aries Agro Ltd (7.07%), and is comparable to Dharmaj Crop Guard Ltd (12.35%). However, it is lower than Best Agrolife Ltd (16.42%) and significantly below India Pesticides Ltd (72.90%).

Objectives of Indogulf Cropsciences IPO

The issue by the IPO will be used by the company for the following purposes:

To secure funds for the company’s working capital requirements;

To pay back or partially pay off existing loans that the company has taken;

To finance the construction of the company’s new in-house dry flowable (DF) plant in Barwasni, Sonipat, Haryana, and;

General corporate purposes.

Indogulf Cropsciences IPO Details

IPO Dates

Indogulf Cropsciences IPO will be open for subscription from June 26, 2025, to June 30, 2025. The allotment of shares to investors will take place on July 1, 2025, and the company will be listed on the NSE and BSE on July 3, 2025.

IPO Issue Price

Indogulf Cropsciences is offering its shares in the price band of Rs 105 to Rs 111 per share. This means you would require an investment of Rs. 14,985 per lot (135 shares) if you are bidding for the IPO at the upper price band.

IPO Size

Indogulf Cropsciences is issuing a total of 1,80,18,017 shares, which are worth Rs 200 crores. Here, 1,44,14,414 shares are through fresh issues, and the remaining 36,03,603 shares are through offer for sale.

IPO Allotment Status

Investors who applied for the IPO can check their IPO allotment status on July 1, 2025, through the registrar's website: Bigshare Services Private Limited, BSE, NSE, or their stockbroker platform.

IPO Listing Date

The shares of Indogulf Cropsciences will be listed on the NSE and BSE on July 3, 2025.

IPO Application Link

Open a demat account with Rupeezy today and enjoy a seamless experience when applying for the IPO. With an easy-to-use platform, Rupeezy makes the IPO application process quick and hassle-free.

Apply for Indogulf Cropsciences IPO

Important IPO Details | |

Bidding Date | June 26, 2025 to June 30, 2025 |

Allotment Date | July 1, 2025 |

Listing Date | July 3, 2025 |

Issue Price | Rs 105 to Rs 111 per share |

Lot Size | 135 Shares |

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

All Category