Is HDB Financial Services IPO Good or Bad - Detailed Review

00:00 / 00:00

HDB Financial Services Limited is kicking off its initial public offering, which will be open from June 25, 2025, to June 27, 2025. While considering applying for this IPO, certain questions may arise in your mind, including whether the HDB Financial Services IPO is good or bad, whether it is worth investing in this IPO, and so on.

This article offers a comprehensive HDB Financial Services IPO review, covering its business operations and fundamental analysis to help you make an informed investment choice.

HDB Financial Services IPO Review

HDB Financial Services Limited, a leading retail-focused NBFC and subsidiary of HDFC Bank, is coming out with its IPO. Classified as an Upper Layer NBFC by the RBI, it ranked 7th in terms of loan book size (Rs. 90,220 crore as of FY24) among peers. The company has a wide customer base of 19.2 million, served through 1,771 branches across 1,170 towns, with strong penetration in underbanked and rural areas.

In FY25, it reported Rs. 1,06,878 crore in gross loans and Rs. 7,446 crore in Net Interest Income. However, PAT declined to Rs. 2,176 crore due to higher credit costs. Key metrics such as ROE (14.72%), ROA (2.16%), and NIM (7.56%) remained healthy. Asset quality weakened slightly, with GNPA rising to 2.26%.

Compared to peers, HDB is smaller in revenue but delivers strong profitability. At the IPO upper band of Rs. 740, its P/E ratio of 27 is cheaper than Bajaj Finance (34.3), Cholamandalam (31.4), and Sundaram Finance (28.1), making the valuation attractive.

HDB Financial Services Limited’s IPO offers a solid mix of scale, profitability, and brand strength at a reasonable valuation. Investors may find this a compelling opportunity in India’s growing NBFC sector, while staying mindful of asset quality and regulatory risks.

Company Overview of HDB Financial Services IPO

HDB Financial Services Limited was incorporated in 2007 and is a leading, diversified, retail-focused non-banking financial company (NBFC) in India, operating as a subsidiary of HDFC Bank Limited. The company is categorized by the Reserve Bank of India as an Upper Layer NBFC (NBFC UL) and ranks as the seventh largest among its peers in terms of Total Gross Loan Book, which stood at Rs 90,220 crore as of March 31, 2024, according to the CRISIL Report.

The company offers a wide range of lending products under three primary business verticals: Enterprise Lending, Asset Finance, and Consumer Finance, serving a growing and diverse customer base primarily consisting of salaried and self-employed individuals, business owners, and entrepreneurs. The company mainly caters to underserved and underbanked customers in low to middle-income households, many of whom have limited or no formal credit history.

Over the years, it has built a strong omni-channel “phygital” distribution model that combines a large physical branch presence with in-house tele-calling operations and an extensive network of external distribution partners. As of March 31, 2025, the company operated 1,771 branches across 1,170 towns and cities in 31 states and union territories, with more than 80% of its branches located outside India’s 20 largest cities and over 70% in Tier 4 and smaller towns.

In addition to its lending business, HDB Financial provides BPO services such as back office support, collections and sales support to its Promoter, HDFC Bank, and distributes fee-based products like insurance. As of March 31, 2025, it had served 19.2 million customers, growing at a CAGR of 25.45% since March 2023, making it the second largest and third fastest growing customer franchise among NBFC peers, according to the CRISIL Report.

Industry Overview of HDB Financial Services IPO

As per the CRISIL Intelligence report, NBFCs in India have significantly evolved in terms of size, operations, technological sophistication, and the range of financial products offered. Their assets under management have expanded from under Rs 2 trillion in Fiscal 2000 to Rs 48 trillion in Fiscal 2025. Within the financial services ecosystem, NBFCs actively compete with banks, micro-finance institutions, digital lending platforms, and informal financiers. Between Fiscals 2019 and 2025, NBFC credit grew at an estimated CAGR of 13.2%. Looking ahead, CRISIL Intelligence projects NBFC credit to grow at a CAGR of 15–17% between Fiscals 2025 and 2028, driven primarily by demand from the retail, MSME, and corporate segments.

Financial Overview of HDB Financial Services IPO

In FY25, HDB Financial Services Limited delivered a steady operational performance, supported by consistent loan book expansion and a broad-based product portfolio.

The company’s Total Gross Loans reached Rs. 1,06,877.58 crore as of March 31, 2025, up from Rs. 90,217.93 crore in FY24 and Rs. 70,030.73 crore in FY23. Net Interest Income stood at Rs. 7,445.64 crore in FY25, marking an increase from Rs. 6,292.04 crore in FY24 and Rs. 5,415.86 crore in FY23. This growth reflects increased disbursements and a healthy asset mix.

However, Profit After Tax (PAT) declined to Rs. 2,175.92 crore in FY25, compared to Rs. 2,460.84 crore in FY24 and Rs. 1,959.35 crore in FY23. The decline was primarily due to increased credit costs, which rose to Rs. 2,113.05 crore from Rs. 1,353.99 crore in FY24.

The company’s Net Interest Margin (NIM) moderated slightly to 7.56% in FY25 from 7.85% in FY24 and 8.25% in FY23, reflecting a rising Average Cost of Borrowings, which increased to 7.90% in FY25, up from 7.53% in FY24 and 6.76% in FY23.

Asset quality showed mixed trends. The Gross Non Performing Assets (GNPA) ratio rose to 2.26% in FY25 from 1.90% in FY24, though improved from 2.73% in FY23. Similarly, Net Non Performing Assets (NNPA) increased to 0.99% in FY25 from 0.63% in FY24. The Provision Coverage Ratio (PCR) decreased to 55.95% in FY25, down from 66.82% in FY24, suggesting a relatively lower buffer against future credit losses.

Despite margin pressure and higher provisioning, the company maintained a healthy Return on Assets (ROA) at 2.16% in FY25, though lower than 3.03% in FY24 and 2.97% in FY23, indicating stable earnings on its asset base.

In summary, FY25 was a year of sustained loan growth and operational scale-up for HDB Financial Services, though profitability was impacted by rising credit costs and funding expenses

Strengths and Risks of HDB Financial Services IPO

Let’s dive into the strengths and weaknesses to assess if the HDB Financial Services IPO is good or bad for investors

Strengths

Rapidly Expanding Customer Base

As of March 31, 2025, the company served 19.2 million customers, growing at a CAGR of 25.45% from FY23 to FY25. Growth is driven by a targeted focus on underbanked but creditworthy segments such as middle-class salaried individuals, small business owners, and self-employed professionals, supported by favorable government policies.Granular and Low-Risk Loan Portfolio

The loan book is highly diversified, with the top 20 customers contributing less than 0.34% of total loans. A strong 11.57% of the portfolio consists of “new to credit” customers, showcasing the company’s advanced underwriting capabilities.Broad and Resilient Product Suite

The company offers 13 loan products across Enterprise Lending, Asset Finance, and Consumer Finance. No single product accounts for over 25% of the loan book. The portfolio has remained resilient through various economic cycles, including COVID-19 and prior financial crises.Strong Growth and Asset Quality

The loan book grew from ?700.3 billion in FY23 to ?1,068.8 billion in FY25 (CAGR 23.54%). Approximately 73% of loans are backed by collateral, with an average tenure of 4 years, supporting healthy asset quality.Robust Liability Franchise and Low Borrowing Costs

With AAA (Stable) ratings from CRISIL and CARE, the company accesses capital at competitive rates. Its average cost of borrowing stood at 7.90% in FY25, backed by a well-diversified mix of funding sources and instruments.

Risks

Increase in non-performing assets and provisioning risk: The company’s Gross Stage 3 Loans increased to 2.26% of Total Gross Loans as of March 31, 2025, from 1.90% in the previous year. Rising defaults, insufficient provisioning, or changes in regulatory norms could adversely affect its financial health and performance.

High exposure to unsecured lending: As of March 31, 2025, unsecured loans accounted for 26.99% of the company’s Total Gross Loans. The absence of collateral backing increases the risk of credit losses in the event of borrower defaults.

Risks associated with secured loan collateral: Secured loans made up 73.01% of the company’s Total Gross Loans as of March 31, 2025. Any decline in collateral value or enforcement delays could hinder recovery efforts and negatively affect the company’s cash flows and profitability.

Potential promoter shareholding reduction due to regulatory changes: HDB Financial Services may be required to reduce promoter shareholding to below 20% if the RBI’s draft circular issued on October 4, 2024, is implemented in its current form. This could materially impact the company’s business operations, financial position, and market valuation.

Strategies of HDB Financial Services IPO

Broaden Product Offerings

The company plans to expand and refine its product portfolio to serve a wider range of customer needs across their financial lifecycle. Recent initiatives, such as automating underwriting for Two-Wheeler Loans, have enhanced efficiency and scalability, enabling broader reach and stronger cross-sell opportunities.Strengthen Distribution Network

The company plans to grow its omni-channel presence by expanding its network beyond the existing 1,771 branches and 140,000+ dealer touchpoints across 1,170 towns. It aims to deepen partnerships with OEMs, retailers, and DSAs to ensure seamless access across urban and rural markets.Leverage Technology and AI

The company plans to increase investments in technology, data analytics, and AI to improve customer experience, operational efficiency, and risk management. These tools will also support better underwriting, collections, cross-sell targeting, and data security.Diversify Funding Sources

The company plans to continue diversifying its funding base to optimize borrowing costs. In FY25, it raised USD 1,050 million through ECBs and will further engage with a broad mix of lenders, including banks, mutual funds, insurers, and pension funds.

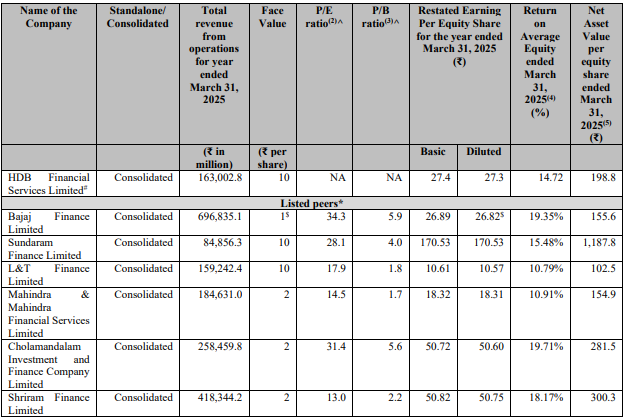

HDB Financial Services IPO Vs Peers

Source: RHP of the company

HDB Financial Services Limited reported Rs. 16,300.28 crore in revenue for FY25, making it smaller in scale compared to listed peers like Bajaj Finance (Rs. 69,683.51 crore) and Shriram Finance (Rs. 41,834.42 crore). However, it delivered a solid ROE of 14.72% and EPS of Rs. 27.4, reflecting strong profitability.

At the IPO upper price band of Rs. 740, HDB’s implied P/E ratio is around 27, which is lower than peers such as Bajaj Finance (34.3), Cholamandalam (31.4), and Sundaram Finance (28.1), indicating a relatively attractive valuation.

Despite its smaller size, HDB outperforms several peers on return metrics, including L&T Finance (ROE 10.79%) and Mahindra Finance (ROE 10.91%), while maintaining operational efficiency and clean asset quality.

Objectives of HDB Financial Services IPO

The fresh issue by the IPO will be used by the company for the following purposes:

To augment the Company’s Tier-I Capital base to support future capital requirements, including onward lending aligned with business growth.

To utilize a portion of the Fresh Issue proceeds for meeting the Offer Expenses.

To gain the benefits of listing, including enhanced brand visibility and the creation of a public market for the Company's equity shares in India.

HDB Financial Services IPO Details

IPO Dates

HDB Financial Services IPO will be open for subscription from June 25, 2025, to June 27, 2025. The allotment of shares to investors will take place on June 30, 2025, and the company will be listed on the NSE and BSE on July 2, 2025.

IPO Issue Price

HDB Financial Services Limited is offering its shares in the price band of Rs 700 to Rs 740 apiece. This means you would require an investment of Rs. 14,800 per lot (20 shares) if you are bidding for the IPO at the upper price band.

IPO Size

HDB Financial Services Limited is issuing a total of 16,89,18,918 shares, aggregating up to Rs. 12,500 crore. This comprises a fresh issue of 3,37,83,783 shares, aggregating up to Rs. 2,500 crore, and an offer for sale of 13,51,35,135 shares, aggregating up to Rs. 10,000 crore.

IPO Allotment Status

Investors who applied for the IPO can check their HDB Financial Services IPO allotment status on June 30, 2025, through the registrar's website: MUFG Intime India Private Limited, BSE, NSE, or their stockbroker platform.

IPO Listing Date

The shares of HDB Financial Services Limited will be listed on the NSE and BSE on July 2, 2025.

IPO Application Link

Open a demat account with Rupeezy today and enjoy a seamless experience when applying for the IPO. With an easy-to-use platform, Rupeezy makes the IPO application process quick and hassle-free.

Apply for HDB Financial Services IPO

Important IPO Details | |

Bidding Date | June 25, 2025 to June 27, 2025 |

Allotment Date | June 30, 2025 |

Listing Date | July 2, 2025 |

Issue Price | Rs 700 to Rs 740 per share |

Lot Size | 20 Shares |

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

All Category