Swiggy vs Zomato FY26 Comparison: Which Stock is More Profitable?

00:00 / 00:00

Summary

|

It took Zomato 18 years to build a business processing $10 billion in annual order value. According to founder Deepinder Goyal, the next $10 billion could take less than two years, as per the recent shareholder’s letter.

That single observation highlights the massive acceleration taking place within India's internet economy.

The Swiggy vs Zomato battle is no longer a basic race to see who delivers food faster. Instead, it has transformed into a high-stakes competition to dominate hyperlocal logistics, determining which platform Indians turn to for instant access to dinner, groceries, event tickets, or everyday essentials.

The financial performance of the full fiscal year 2026 revealed something surprising.

While Blinkit is winning the race for pure market expansion, Swiggy is quietly fighting a different battle altogether by prioritizing its structural bottom line.

The Real Story Is Quick Commerce

Food delivery built both companies. Quick commerce is completely redefining them.

The strongest evidence comes directly from the annual numbers.

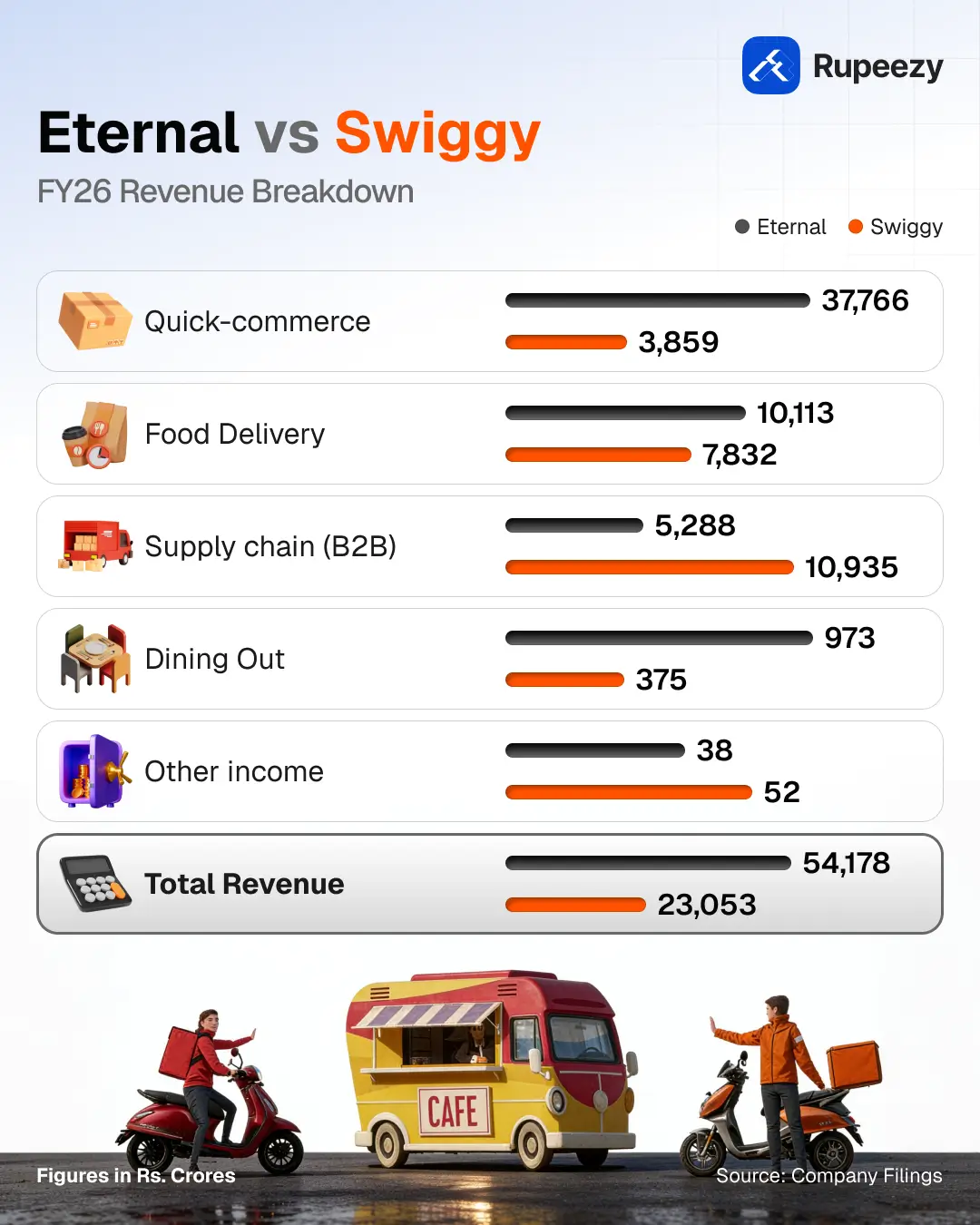

For the full year FY26, Swiggy's operations reached a massive milestone, pushing its total consolidated revenue from operations up 51.3% year-on-year to Rs 23,060 crore, fuelled heavily by an 81.1% surge in its quick-commerce revenue engine, according to Swiggy’s FY26 financial disclosures.

Concurrently, Zomato’s multi-brand corporate parent ecosystem, operating under its newly structured parent name, Eternal, reported a massive surge in full-year consolidated revenue from operations, which jumped 169% year-on-year to Rs 54,364 crore.

This explosive growth was driven primarily by Blinkit's transition to a high-velocity inventory-led category model, officially outscaling the operational growth curve of the core food delivery business over the full fiscal year.

For the first time, the future of both companies may depend more on groceries than restaurants.

Blinkit Is Winning The Scale Race

If there is one KPI that explains Blinkit's lead, it is aggressive dark store infrastructure.

Blinkit ended FY26 with a massive network of 2,243 stores, compared to Instamart's 1,143 dark stores operating across 129 cities.

Why is that important?

A more dense network of physical locations triggers a flywheel effect: better product selection, faster delivery, and deeper penetration into new markets.

Blinkit is already benefiting from this advantage. In FY26, the company scaled to a point where over 109 million unique Indian consumers transacted across the ecosystem. This allowed the quick-commerce arm to secure consistent operational milestones, proving that dense cluster scale and absolute market penetration can coexist.

Swiggy Is Solving The Harder Problem

While Blinkit is expanding aggressively, Swiggy is focusing on something less visible but equally important: Unit Economics and Long-Term Sustainability.

CEO Sriharsha Majety believes quick commerce is becoming increasingly commoditised and that long-term success will come through brand differentiation rather than burning capital in price wars.

The primary engine driving this focus on unit economics is Swiggy's aggressive expansion of its private label, Noice. By scaling Noice to hundreds of SKUs across high-margin categories like artisanal bakery items, premium snacks, and fresh staples, Instamart is planning to gain from high gross margins from FMCG brands.

The annual numbers support that strategy.

According to Swiggy's full-year fiscal statement, the brand successfully narrowed its net operational cash burn in key areas, scaling its annual consolidated adjusted revenue to Rs 24,315 crore.

The new strategy may not generate the same excitement as rapid store expansion, but they address the biggest question surrounding quick commerce:

Can this business eventually become profitable?

For investors following Swiggy's revenue growth, that question may become more important than raw expansion, especially as Swiggy operates under recent post-IPO public market scrutiny.

The KPIs That Explain Who Is Really Winning

Revenue gets attention.

Store count gets headlines.

But Key Performance Indicators (KPIs) reveal what is happening beneath the surface.

Store Network

Blinkit's 2,243 stores give it a significant advantage over Instamart's 1,143 stores. This larger network helps improve delivery speed, expand product assortment, and strengthen market penetration.

Monthly Transacting Users (MTUs)

For FY26, Swiggy’s scaled user base hit a consistent upswing, culminating in a platform-wide average of 25.2 million Monthly Transacting Users. Eternal counterbalanced this by expanding its unique consumer reach to over 100 million transacting users across its multi-app super-brand ecosystem over the 12 months, as highlighted in its Annual Shareholder Letter.

Why does this matter?

Because quick commerce is ultimately a habit business. The platform that becomes part of a consumer's weekly shopping routine gains stronger retention and higher lifetime value.

Average Order Value (AOV)

Throughout the fiscal year, a noticeable shift occurred in basket economics. Instamart's baseline Average Order Value (AOV) settled at Rs 700. Conversely, Eternal witnessed a drop to a net AOV of Rs 525 for its Blinkit division over the same period.

Profitability

For FY26, Eternal turned a major corner, reporting a consolidated annual profit of Rs 366 crore.

Swiggy, conversely, is playing a calculated long game. At the same time, its total annual consolidated loss stood at Rs 4,154 crore due to deep market infrastructure investments. Its underlying segments, particularly its Out-of-Home consumption business, have recorded their first full fiscal year of positive adjusted profitability.

One company is proving that scale can drive annual profitability.

The other is proving that losses can be curbed while building structural business value.

Where Is The Revenue Coming From?

One of the biggest changes visible in FY26 is revenue diversification. Five years ago, both companies were largely food-delivery businesses.

Today, they are building complete convenience ecosystems.

For Swiggy, a diversified mix across the core food delivery business, Instamart, Dineout, and Supply Chain & Distribution (Assure) form multi-layered revenue engines.

For Eternal, Blinkit, Hyperpure, District, and Zomato are doing the same.

This diversification reduces dependence on a single business and creates new opportunities for long-term growth.

The Bigger Threat Nobody Can Ignore

The race is not limited to Swiggy and Zomato.

Players like Zepto, BigBasket, and Flipkart are investing aggressively in quick commerce.

That means market leadership will not be decided by growth alone.

It will be decided by who can balance scale, profitability, customer retention, and operational efficiency at the same time.

Who Is Actually Winning?

The answer depends on which KPI you value the most.

If scale is the priority, Blinkit is clearly ahead.

If improving economics is the priority, Swiggy is making meaningful progress.

Eternal is betting that infrastructure and expansion create long-term advantages.

Swiggy is betting that differentiation and stronger unit economics will ultimately matter more.

At the moment, Blinkit appears to have the lead. But FY26 also showed that Instamart is quietly closing important gaps.

If you are tracking these market movements to take equity exposure or rebalance your portfolio in India's fast-evolving internet economy, you can open an account and trade seamlessly using Rupeezy to capitalize on these quick commerce trends.

And that is why the Swiggy vs Zomato story is far from over.

The content on this blog is for educational purposes only and should not be considered investment advice. While we strive for accuracy, some information may contain errors or delays in updates.

Mentions of stocks or investment products are solely for informational purposes and do not constitute recommendations. Investors should conduct their own research before making any decisions.

Investing in financial markets are subject to market risks, and past performance does not guarantee future results. It is advisable to consult a qualified financial professional, review official documents, and verify information independently before making investment decisions.

Open Rupeezy account now. It is free and 100% secure.

Start Stock Investment

All Category