Invest in Mutual Funds

Your goals deserve better growth — start investing today

Browse All Mutual Funds

| Fund Name | Return | Risk | Cat. Avg |

U UTI Silver ETF Fund of Fund OtherFoFs (Domestic) | 46.61% | 37.41% | -% |

K Kotak Silver ETF Fund of Fund OtherFoFs (Domestic) | 46.56% | 36.99% | -% |

A Axis Silver Fund of Fund OtherFoFs (Domestic) | 46.53% | 37.39% | -% |

I ICICI Prudential Silver ETF FOF OtherFoFs (Domestic) | 46.47% | 36.92% | -% |

H HDFC Silver ETF Fund of Fund OtherFoFs (Domestic) | 46.36% | 39.55% | -% |

A Aditya Birla Sun Life Silver ETF Fund of Fund OtherFoFs (Domestic) | 46.24% | 37.75% | -% |

N Nippon India Silver ETF Fund of Fund OtherFoFs (Domestic) | 46.13% | 42.98% | -% |

H HDFC Defence Fund EquityThematic Fund | 41.03% | --% | -% |

E Edelweiss Gold and Silver ETF Fund of Fund OtherFoFs | 40.83% | 26.98% | -% |

M Motilal Oswal Gold and Silver Passive Fund of Funds OtherFoFs | 38.16% | 25.93% | -% |

Mutual Fund Categories

Select from 1500+ funds across equity, debt and hybrid categories.

Discover the Best Funds and AMCs for Your Portfolio

Invest in mutual funds with data-backed analysis. No instinct, trust numbers

Benefits of Investing in Mutual Funds with Rupeezy

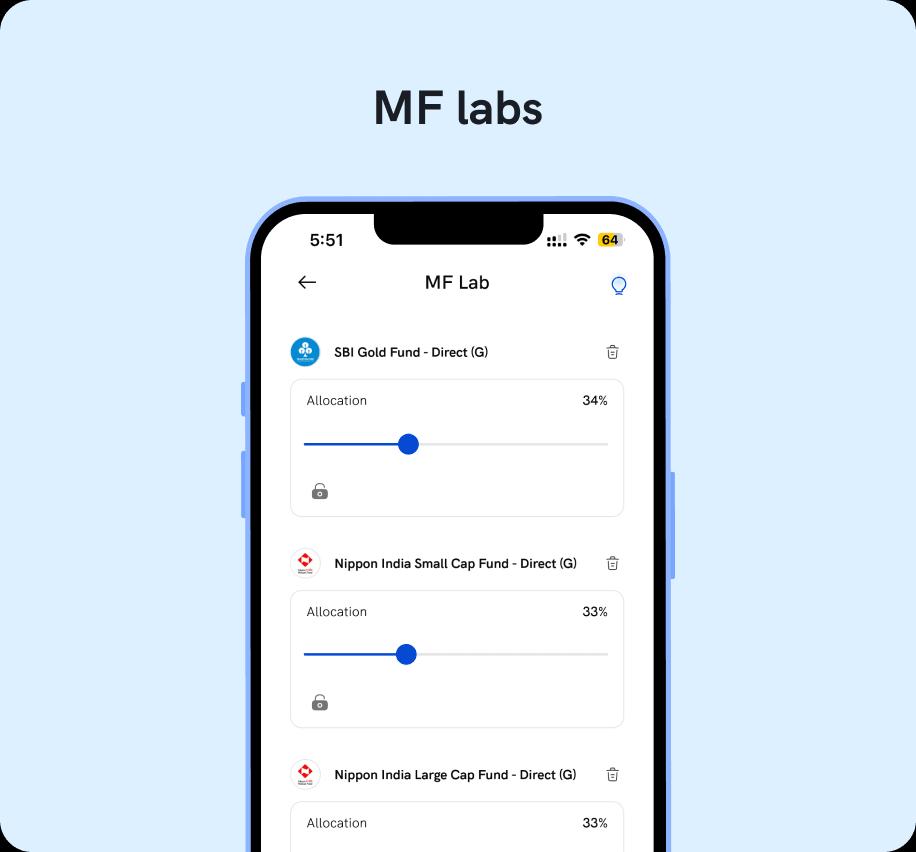

MF Lab

Back test your mutual fund allocations before investing

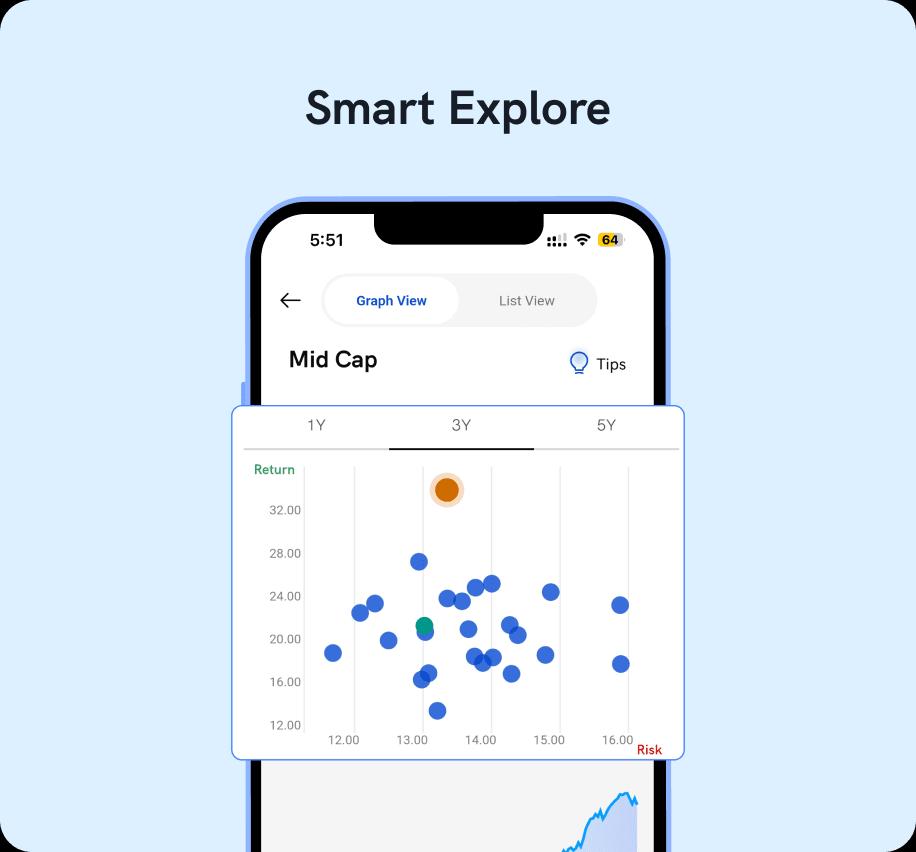

Smart Explore

Quickly compare risk & return of multiple mutual funds in one look

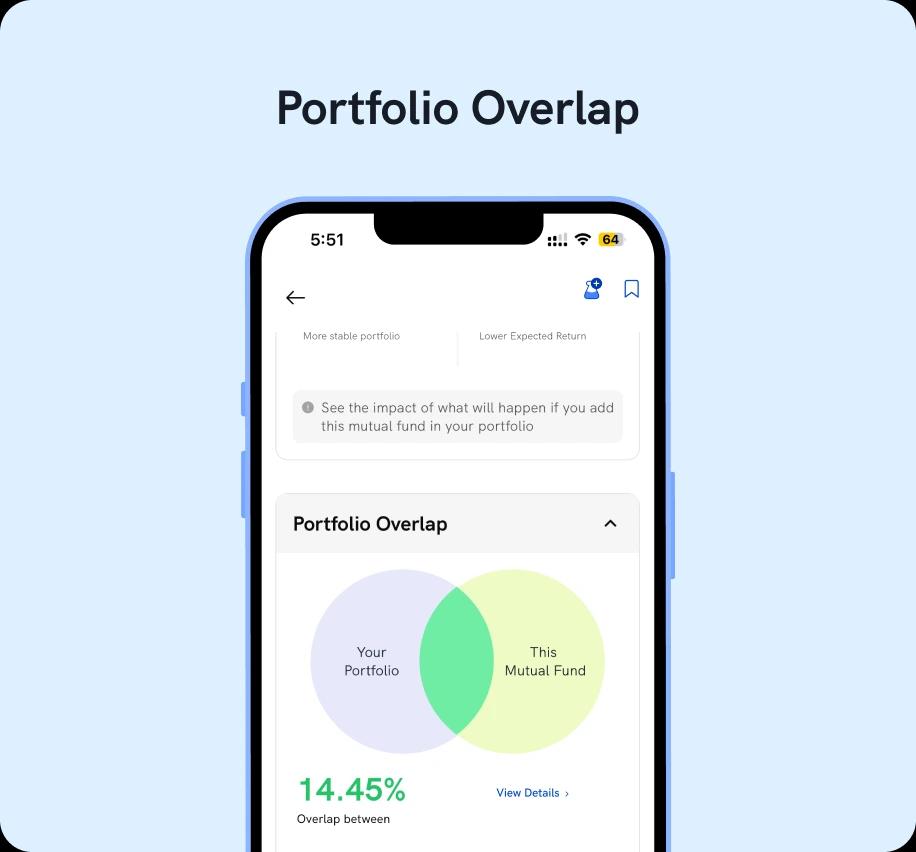

Impact Analysis & Portfolio Overlap

Make your portfolio truly diversified by checking the overlap before buying a new mutual fund

MF Lab

Back test your mutual fund allocations before investing

Smart Explore

Quickly compare risk & return of multiple mutual funds in one look

One Stop Solution for

Mutual Funds

SIP with Automated Payment

Set up SIPs with auto debit option

Flexible SIP Options

Choose weekly, monthly, or quarterly SIPs to fit your schedule

One Click Import

Import and track your existing mutual fund portfolio to Rupeezy

Step Up SIP

Add a little extra topping of SIP every year to beat inflation

Speedy Investment

Quick Pay with UPI or Net banking

How to Invest in Mutual Fund Through Rupeezy

App

Add KYC details such as PAN, DOB, and

Add KYC details such as PAN, DOB, and complete account verification.

Invest in a click, set up

Invest in a click, set up SIPs, pay with UPI or

Net Banking